More than $8.72 billion in Bitcoin and Ethereum options expired today, making it the biggest derivatives event of February.

Cryptocurrency markets are at a critical inflection point, with increased volatility and fragile sentiment as option expirations approach.

February’s $8.72 billion expiration crossroads: Will Bitcoin and Ethereum face painful trading?

Bitcoin accounts for the majority of the exposure, with 114,705 contracts with a total notional amount of $7.74 billion awaiting settlement.

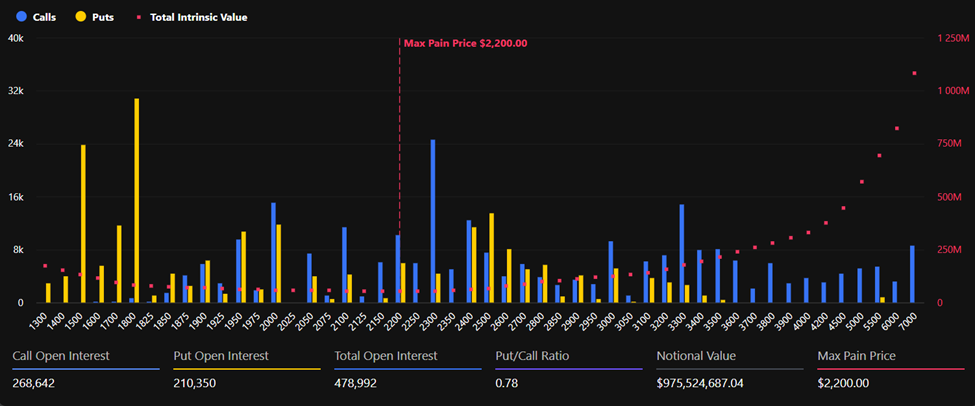

Ethereum follows with 478,992 contracts worth approximately $975 million. In total, maturities account for approximately 20% of total open interest, suggesting potential market impact.

At their current prices, both assets are significantly below their respective “max pain” levels, or strike prices at which most options become worthless.

Bitcoin was trading at $68,052, compared to its maximum pain level of $75,000. Ethereum changes hands around $2,035, below the maximum pain threshold of $2,200.

Call open interest (OI) is dominant across both assets. Bitcoin has 66,300 call contracts compared to 48,405 puts, giving a put-to-call ratio of 0.73. Ethereum has a ratio of 0.78, with 268,642 calls and 210,350 puts.

Analysts at Deribit point out that call OI leads across both majors, with Bitcoin assuming a large assumed share in payments. This factor can amplify spot sensitivity when hedge flows are strengthened.

Divergence in volatility is a signal of anxiety

Volatility indicators, on the other hand, reveal a more nuanced picture. According to Deribit data, Bitcoin’s DVOL index is 53 and its implied volatility (IV) percentile is 87.7, which is up compared to its historical range.

Ethereum’s DVOL is high in absolute terms at 70, but its IV percentile of 55.7 suggests it is not as extreme as past behavior.

Still, Ethereum’s volatility is around 15-20 points higher than Bitcoin across the curve. This indicates that traders are pricing in significantly higher uncertainty across ETH’s maturity.

The term structure for both assets remains contango, with front-end volatility premiums concentrated around the February expiration.

Fear eases, but conviction is delayed.

Earlier this month, the 25 delta skew for both Bitcoin and Ethereum plummeted towards -30, reflecting strong demand for downside protection as prices plummeted.

Since then, the skew has steadily recovered to around -8 to -9, indicating that panic hedging has eased. However, the skew remains negative, indicating that the market has not fully emerged from its defensive stance. Against this backdrop, analysts at Greeks.live say the overall market is depressed.

In early February, Bitcoin briefly tested the psychological threshold of $60,000, but has since remained weak above it.

Although implied volatility has increased during the recent two-day rally (47% key period IV for BTC and 65% for ETH), confidence remains thin.

“Although the downward price trend has eased, market confidence remains insufficient,” Greeks.live said, adding that large call options have dominated recent trading activity, especially at medium- and long-term maturities.

While the recovery in the skew indicator signals a rise in bottom fishing activity, the company warns that the market remains firmly in bear territory.

Importantly, analysts argue that the crypto market lacks new capital inflows and clear catalysts, with pessimistic discourse still dominating social channels. Despite signs that extreme fears are easing, the confidence behind the rebound appears tentative.

With both Bitcoin and Ethereum trading well below their maximum pain levels, spot prices could rise heading into today’s option expiration. Such an outcome could intensify potential ‘pain trading’.

However, with subdued demand, derivatives markets are pricing in less panic and volatility may reduce after expiration, but confidence has yet to return.