While Bitcoin and some of the top cryptocurrencies are rising, most altcoins are falling. Even as the top 200 assets continue to grow, the decline in the cumulative accumulation/distribution (A/D) line in the broader crypto market has created a noticeable divergence.

This “K-shaped” market pattern reflects the deepening divergence between crypto sectors. Winners are making compounding profits, but many assets are quietly losing value. The same trends are evident across the broader U.S. economy and traditional markets, highlighting growing polarization.

sponsored

Market width shrinks as capital concentrates in leader companies

The performance of the cryptocurrency market is now driven by fewer assets. Analyst Jamie Coutts pointed out that altcoins have been in a bear market since 2021. The A/D indicator, developed by Mark Chaikin, measures money flow through price and volume. This clearly shows the difference.

Although the A/D lines of all cryptocurrencies are declining, the top 200 assets are showing a steady upward pattern. This shift suggests that institutional and retail capital are increasingly integrated into established projects. As a result, unadopted chains and applications struggle with supply pressure and reduced incentives.

“Breadth has been collapsing for years now. Fewer assets are working, and most are being quietly leaked out. If chains and apps don’t get real adoption, they won’t survive,” Jamie Coutts posted.

These indicators highlight the transformation of the cryptocurrency market. Projects built on the 2021 bull market narrative and token incentives are now facing challenges as liquidity moves to assets with simple utility. This process clearly distinguishes which projects are sustainable and which will languish under a speculation-driven model.

sponsored

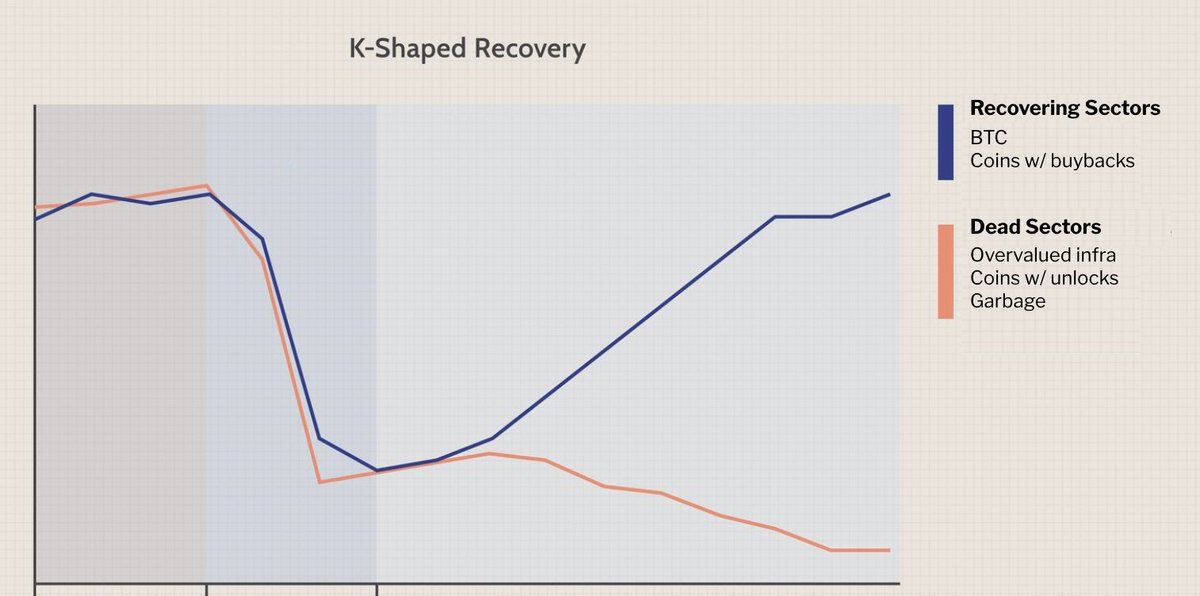

Defining winners and losers in a K-shaped market

This pattern has implications for more than just asset rankings. Analyst Taiki Maeda said the recovery was K-shaped. Bitcoin and cryptocurrencies with buyback models form a rising field, benefiting from scarcity and strong incentives.

On the other hand, infrastructure tokens that are unlock-heavy or lack value propositions will fall. This shift signals a maturation of the market, with users seeking assets based on utility rather than hype. The artificial intelligence sector is attracting notable investments and developer attention, further distinguishing successful projects from the rest.

sponsored

Tokenization and the real-world asset sector are also gaining traction. Traditional financial institutions are exploring blockchain solutions, offering use cases that bring together traditional finance and decentralized technology. Still, most altcoins remain outside these trends and struggle as capital is allocated more selectively.

The A/D indicator remains a powerful trend finding tool. The Technical Analysis Guide explains that it is more reliable than volume-only indicators in identifying actual buying and selling pressure because it tracks the closing price during each period. A rising A/D line indicates accumulation and a falling line indicates distribution. If the price and A/D diverge, a reversal may occur.

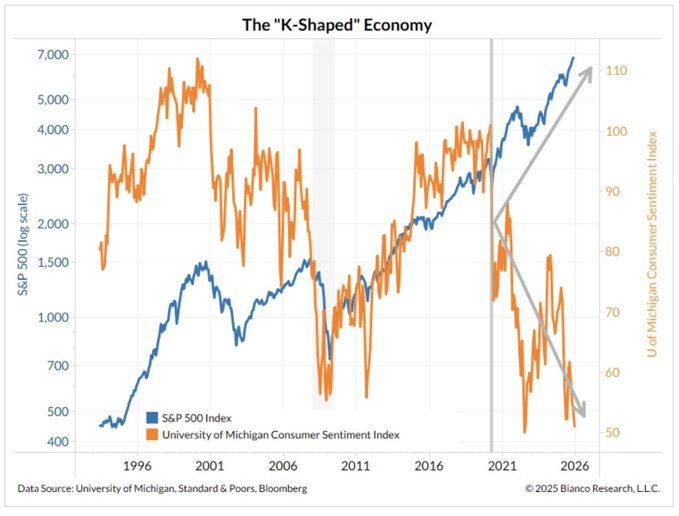

Macro factors deepen the rift in cryptocurrencies

This K-shaped pattern also reflects global macroeconomic trends. In the US, the S&P 500 has risen since 2021, but the Consumer Sentiment Index has declined, suggesting asset owners are thriving as sentiment weakens.

sponsored

“We live in a K-shaped economy. Consumer sentiment is collapsing while asset owners continue to compound interest. This means the rich economy is booming while the livelihood economy is suffering,” PolymarketMoney posted.

This environment directly forms digital assets. Cryptocurrencies are seen as stores of value or inflation hedges, attracting capital seeking refuge from currency risk. In contrast, speculative tokens with no clear value face losses as investors seek real utility rather than just a story.

As correlations between sectors change, broad altcoin diversification no longer protects your portfolio. Investors now prefer to focus on assets with proven fundamentals, a change from earlier cycles when broad exposure paid off. Market rotation is accelerating and only solid projects can maintain momentum.

By January 2026, the key question for investors is how long this K-shaped divergence will last. The forces behind this division show little sign of abating. It remains to be seen whether this will support a healthier ecosystem by narrowing the focus, or risk stifling innovation by concentrating resources. For those operating in these markets, continuous monitoring throughout the year is important.