Even the safest areas of the market can start to feel uneasy as oil prices soar, wars drag on, and investors begin to suspect that inflation is moving back in the wrong direction.

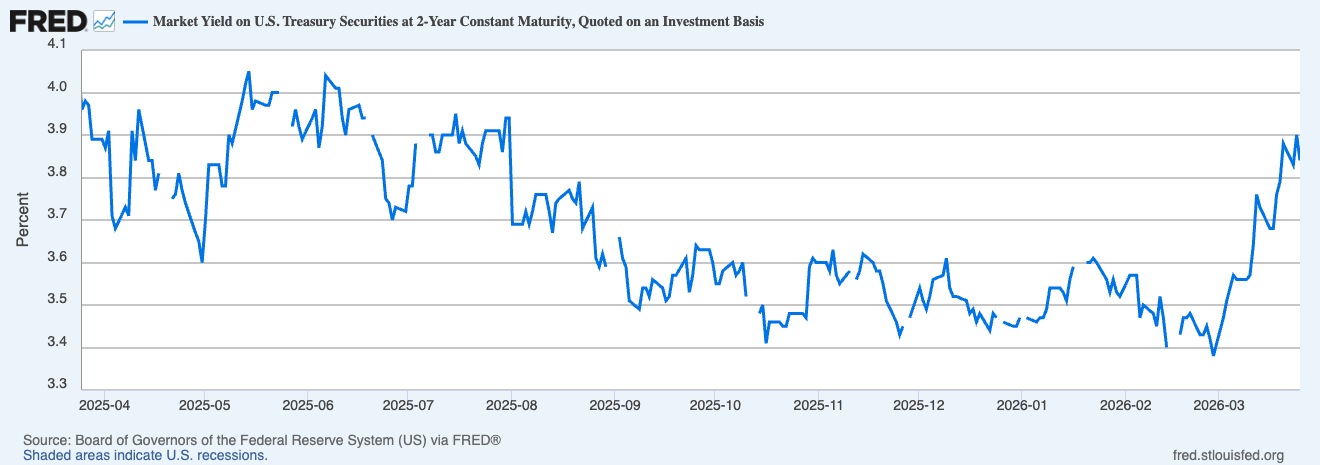

That was the message from Tuesday’s sale of two-year U.S. bonds. These are short-term Treasuries that are widely watched because they reflect what investors think could happen over the next few years, especially with regard to Federal Reserve interest rates.

When demand for these short-term bonds is strong, it shows that professional and institutional investors believe that inflation will ease and eventually policy will ease.

Therefore, when demand weakens, the signal also changes. Investors are demanding better compensation and are preparing for a difficult road ahead.

Tuesday’s auction fell into that second category. The Treasury sold $69 billion worth of two-year bonds at a high yield of 3.936%, but demand was weaker than last month. Although the bidding ratio fell to 2.44 times from 2.63 times in February, primary dealers ended up accounting for a large share of sales.

These numbers indicate that investors were less willing than usual to lend money to the U.S. government at an interest rate of 3.9% for just two years.

The soft selloff comes just as oil prices have risen due to conflicts in the Middle East and hopes for an early interest rate cut from the US Federal Reserve are beginning to fade. Despite an acceleration in costs and selling prices, U.S. business activity slowed to an 11-month low in March, leaving investors staring at a rather unpleasant economic picture.

Two-year U.S. Treasuries are one of the market’s best indicators of where investors think interest rates will go in the near future. The weak bids indicate traders are not convinced the Fed can ease policy anytime soon. It could also be a sign that inflation concerns are starting to outweigh the normal instinct to rush into government debt during geopolitical shocks.

Why this simple auction raised a red flag

For much of last year, investors were hoping to see light at the end of the tunnel. Inflation appears to be trending down and growth is cooling in an orderly manner, which could eventually give the Fed room to cut rates. Short-term Treasuries are a good fit for this recovering market as they provide a good position for future easing.

However, all this has come crashing down with the recent oil crisis. Oil prices have soared, impacting gasoline and broader business costs as the Iran conflict threatens to escalate into an all-out war in the Middle East. This nullified any previously seen softening in business activity and left markets grappling with the prospect that the economy could slow while inflation rises. If this combination comes to fruition, the Fed will not be able to offer any cheap bailouts for the next year or so.

Once you start thinking about this as a real possibility, the meaning of a “safe” asset changes.

While the relative safety of assets is still important in this situation, inflation is even more important.

Investors are beginning to question whether holding two-year Treasuries at a given yield really provides enough protection if energy prices rise and the path to lower interest rates appears uncertain. This is why this week’s slump in demand has garnered so much attention. That showed the market was hoping for more gains before intervening.

The Fed’s rhetoric has increased that fear. Fed President Michael Barr said policymakers may need to keep interest rates on hold for a while because inflation remains above target and conflicts in the Middle East have heightened upside risks through energy.

Comments like this help explain why two-year Treasuries are so important. Two-year Treasuries are the part of the U.S. Treasury market most closely tied to the next chapter of Fed policy. When it starts to wobble, investors typically react to what they think central banks may or may not be able to do next.

What signals say about the economy from here on

This month’s auction was a wake-up call for the coming months.

Investors are starting to examine whether the old assumption still holds true: If oil prices remain high, can inflation continue to ease? If energy costs start to push prices higher, could the Fed cut rates?

The answers to these questions affect everyone, not just buyers of U.S. Treasuries.

Rising short-term yields could tighten financial conditions, put pressure on valuations in other markets, and raise the bar for risk-taking in stocks and speculative assets as a whole. Expectations about the Fed’s future policy factor into all kinds of pricing decisions and could potentially change the terms of borrowing.

That’s why a weak auction at the front of the curve could tell a larger story about confidence, fear, and how investors see the next phase of the economy shaping up.

There is still room to cool this signal down. Oil prices have fallen slightly on hopes of a ceasefire, a move that could ease some pressure on inflation expectations.

Nevertheless, the market is still arguing with itself, and that argument is alive in every new oil headline, every Fed statement, and every new article about prices and growth.

For now, the message from the auction is clear. Investors are looking ahead to the next two years, and they see a tougher road ahead than they saw a month ago. They see war, oil, inflation, slow economic activity, and less room for the Fed to bail out than the market expected. And we’ve seen glimpses of markets starting to price in a more difficult world.