Artificial intelligence and crypto-native tools are rapidly shaping a future where software agents can self-fund, execute cross-chain strategies, and move through financial markets without anyone controlling them.

According to a recent report by DWF Ventures, automated agent activity now accounts for an estimated 19% of all on-chain transactions, with 17,000 agents launched since 2025.

The report added that the agent economy is already here.

For now, most of this machine-driven money movement is done through bots that shuffle stablecoins across a patchwork of payment systems that still rely on centralized gateways, managed issuers, and rails linked to cards.

Crypto is building an interface for machine payments before building out the autonomy that the interface is supposed to enable.

Headlines about “AI agents” spending crypto suggest a new autonomous machine economy, but the underlying flows still look like bot-driven plumbing controlled by familiar intermediaries. This gap will determine who collects the fees, how much demand there actually is for crypto rails, and whether this trend ultimately strengthens DeFi or simply widens the reach of the dollar system.

actual working machine

Before treating DWF’s 19% figure as a definitive measure of self-financing, it helps to understand what DWF actually measures.

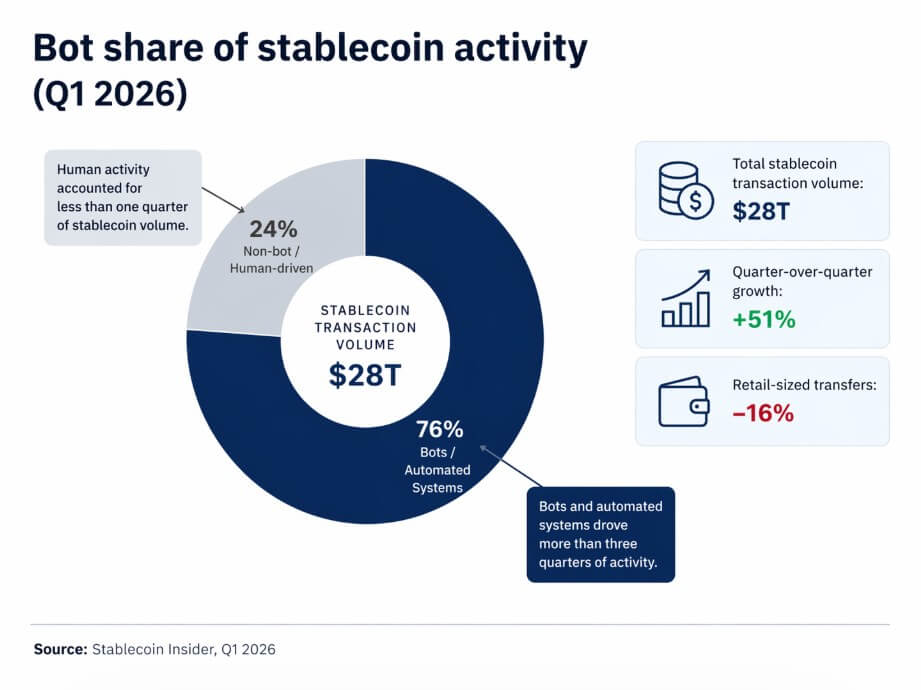

According to Stablecoin Insider data for the first quarter of 2026, bots accounted for approximately 76% of stablecoin trading volume, and total stablecoin trading volume reached $28 trillion, an increase of 51% from the previous quarter.

Retail remittances fell by 16% over the same period, the largest decline on record.

Automation, routing, and high frequency machine activity drove its growth. Software systems that programmatically move funds between exchanges, wallets, liquidity venues, and payment intermediaries constitute the currently visible form of the machine economy.

Stablecoins are a natural fit here. Prices don’t fluctuate, settle on programmable rails, and use the same units of account that most software already understands. Stablecoins make sense for automated systems that need to move money without worrying about currency risk.

DefiLlama currently estimates the stablecoin market to be around $320 billion, with Ethereum accounting for around 52% of the supply, Tron overwhelmingly USDT at $86.7 billion, Solana led by USDC at $15.7 billion, and USDC at a base of $4.9 billion.

The blockchain leading the flow of machine-driven stablecoins is one that is already being built to move dollar tokens at scale. In many ways, stablecoins are becoming the first money rails used not only by people but also by software.

hybrid design

Machine commerce payment standards are beginning to take shape. x402, Stripe’s Machine Payments Protocol (launching in March 2026), and Google Cloud’s Agent Payment Protocol 2 are all signs that this space is really gaining momentum.

Current machine payments infrastructure Full autonomy requires Support for stable coin transfers Self-funding and fund management by agents Calling of agents between agents or by humans Independent execution without human approval Payments through card-linked or bank-linked intermediaries Native on-chain payments end-to-end Managed issuer and centralized gateway Decentralized trust and identity system Compliance and custody handled by intermediaries Built-in reputation, insurance, and fail-safe hybrid payment standards (x402, MPP, AP2) Autonomous optimization across evolving market conditions

The x402 Foundation, which launched under the Linux Foundation in April 2026, includes Coinbase, Cloudflare, Stripe, Google, and Visa as participants.

Still, x402’s public dashboard shows about 75 million transactions and $24 million in trade value over the past 30 days, a far smaller amount compared to the trillions of dollars already flowing through stablecoins.

Stripe’s x402 implementation goes through a Stripe-managed deposit address and capture flow, while Google’s AP2 explicitly supports cards and real-time bank transfers, along with stablecoins.

Artemis reports that crypto card transaction volume has grown from around $100 million per month in early 2023 to more than $1.5 billion per month by the end of 2025, but is still largely settled through fiat rails.

Current infrastructure builds programmable machine-to-money interfaces on top of centralized systems.

Visa’s US stablecoin payment products will reach annual circulation of $3.5 billion by the end of 2025. In April, the company joined Tempo as a blockchain validator designed for proxy commerce.

Visa’s latest move confirms that the agent economy’s most active builders are designing for hybrid rail.

DWF’s own report concludes that true end-to-end autonomy is yet to be achieved, and the architecture explains why.

Fully autonomous agents in financial markets require verifiable identities, custodial regimes that tolerate model errors, reputation systems that allow counterparty credit extension, fail-safe mechanisms that include damages, and capital flows that do not rely on human replenishment.

None of these layers exist at production scale. DWF performance data supports the finding that while agents perform better on narrow rule-based tasks such as yield optimization, humans still perform better in more complex trading situations.

Today’s machine economy functions as automation of well-defined workflows. The conditions for independent financial decision-making, such as verifiable identity, custody, reputation systems, and fail-safe execution, have not yet converged at production scale.

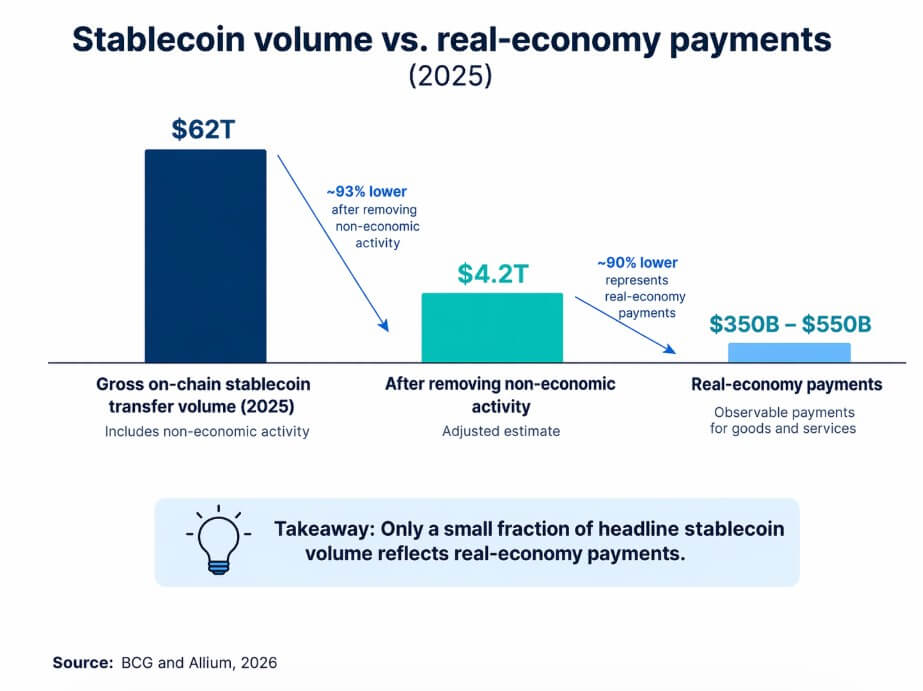

Chainalysis adds that bot activity, MEV, liquidity provisioning, and internal operational transfers will inflate the raw stablecoin volume.

BCG and Allium estimate that of the approximately $62 trillion in total on-chain stablecoin transfers in 2025, only $4.2 trillion will remain after removing non-economic activity, and only $350 billion to $550 billion will result in payments in the real economy.

Much of what is registered as mechanical trade is still market plumbing.

There are two paths from here

The bull case is that payment standards converge, regulated stablecoin issuers expand, and machine-to-machine payment flows move from proof of concept to production.

The stablecoin market capitalization, currently close to $320 billion, approaches the projected ceiling of $2.3 trillion by 2030, and adjusted payment activity is consistent with Chainalysis’s high-growth scenario in which stablecoin transaction volume begins to converge with Visa and Mastercard transaction volume over the next decade.

Platforms that combine trusted identities, compliant dollar liquidity, and low-friction orchestration across on-chain and off-chain services are moving forward.

The agent economy becomes the story of a payment infrastructure running on crypto rails that most users do not consciously interact with as cryptocurrencies.

The bearish case more closely aligns with today’s data. Stablecoin bot volume is still growing, but most of it is not converted into durable real economy machine commerce.

Card networks and banking intermediaries absorb most of the demand for machine-readable payments without distributing anything, and regulatory costs concentrate business among large incumbents.

Stablecoins primarily grow through exchange collateral, treasury liquidity, and payment middleware. Today’s centralized infrastructure still constrains the funding of programmable machines at full economic scale.

BCG and Allium’s findings that the total volume of stablecoins equivalent to payments in the real economy in 2025 was only $350 billion to $550 billion supports this reading. The base is much smaller than the headline numbers suggest, and the distance between the current stack and a true autonomous agent economy is wider than the marketing pitch realises.

rail problems

The deeper debates playing out through all of this center around who will process machine payments and where the trust will be once the flow of programmable dollars reaches meaningful economic scale.

Stripe, Visa, Google, and regulated stablecoin issuers are running that race at least as much as other crypto-native agent platforms.

Stablecoin issuers hold about 53% of their assets in Treasury bills, and their holdings have grown to about $70 billion since 2022, according to Treasury data.

Each step-by-step introduction of machine-driven stablecoins will increase demand for short-term U.S. government debt and embed dollar-denominated payment standards into automated systems around the world.

The agent economy as currently constructed is more of a story of dollar expansion, and the companies best placed to control the rails are the same companies that already control the pipes.