Pump.fun has built one of the fastest meme token liquidity machines in cryptocurrencies. Now, on July 12th, its own token is facing the kind of liquidity test the platform typically creates for other tokens.

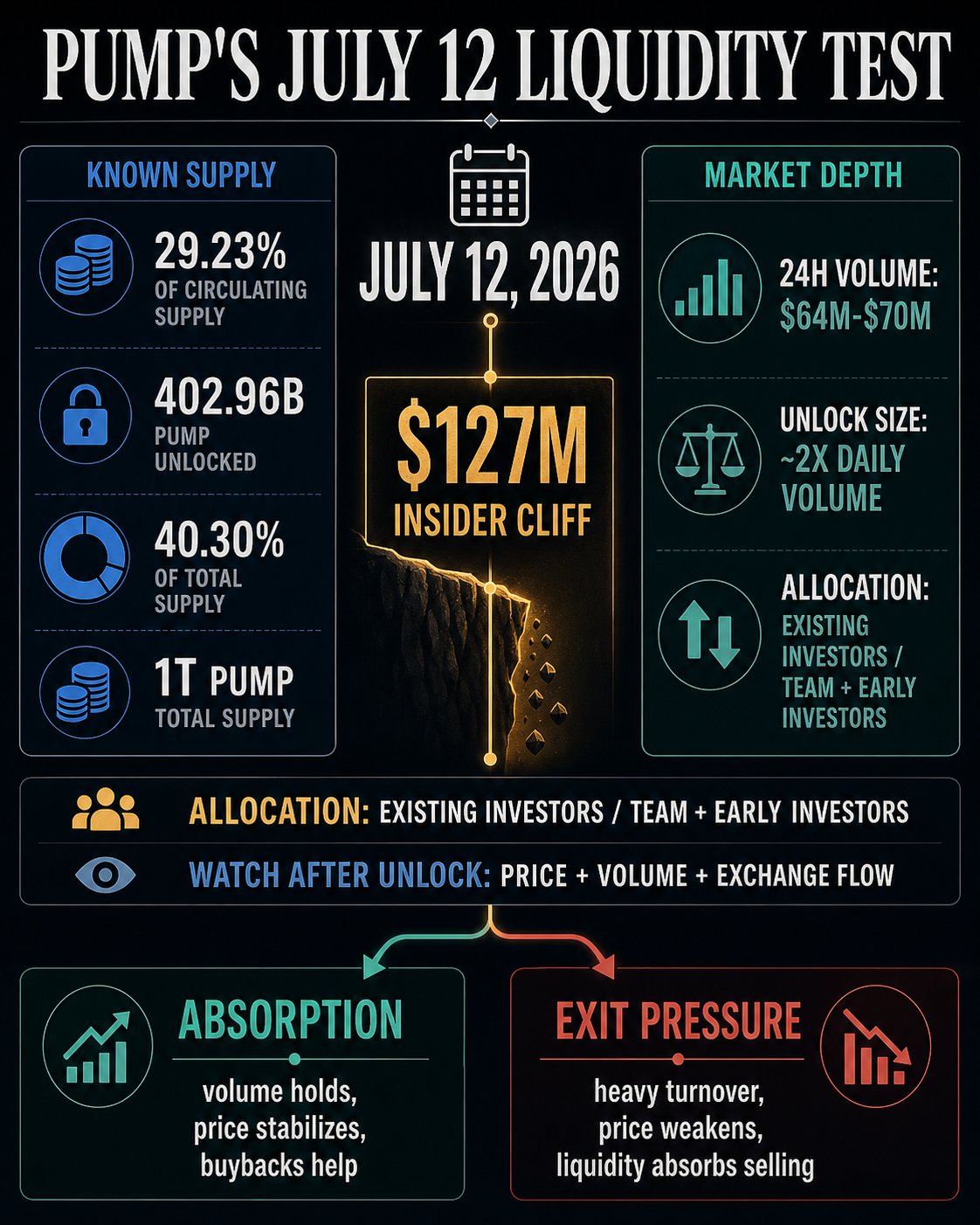

The platform’s PUMP token is scheduled to be unlocked on July 12th, and Tokenomist values it at $127 million, representing 29.23% of the circulating supply.

Scheduled releases are associated with insider assignments. Tokenomist’s weekly unlock digest explains that tranches will flow to the team and early investors, while the PUMP vesting page identifies the next release to be existing investors.

This is important as PUMP has recently faced a large release schedule against an order book that has shown daily sales much lower than its unlocked size.

The CryptoSlate market page shows PUMP trading around $0.00155 on July 8, with 24-hour volume ranging from roughly $64 million to $70 million across the PUMP asset page and broader coin rankings.

Therefore, the expected cliff, before adjusting for how much unlocked allocation is actually sold, is close to twice the recent visible daily volume.

If the recipient holds it, the full $127 million may not remain on the exchange. The unlock size simply sets the maximum amount of new supply available. Sell-through determines pressure.

However, this token is entering a more direct liquidity test than most meme coin narratives produce. If held by the recipient, demand could absorb the date. If sold to weak levels, the unlock could turn from a calendar entry to visible exit pressure.

Why is PUMP unlock done in one block?

According to Tokenomist’s vesting page, approximately 402.96 billion PUMP, representing 40.30% of the token’s 1 trillion supply, has already been unlocked. The remaining supply will continue to be governed by the project’s vesting schedule, which runs through 2029.

The same page states that Pump.fun uses cliff vesting for most of its assignments. This means that tokens are released in large scheduled blocks, rather than being rolled smoothly into the market over time.

That’s why the events of July 12 are more than a footnote in Tokenomics. Cliff structures concentrate risk on dates that traders can see in advance.

Traders can price them, hedge them, ignore them, or use them as liquidity windows. Supply still arrives in visible blocks.

Future releases will also include tokens whose float is still maturing. Tokenomist has 33% of its allocation going to the initial coin offering, 24% to community and ecosystem initiatives, 20% to the team, 13% to existing investors, 3% to live streaming, 2.6% to liquidity and exchanges, 2.4% to ecosystem funds, and 2% to foundations. This combination will result in a significant proportion of future supply in the category, which has the potential to create market confidence.

The strongest bearish case is simple. Large blocks of insider-controlled PUMP become available while the daily trading volume of the token is lower than the scheduled release volume.

Even if a significant portion of that allocation requires liquidity, buyers should absorb it without demanding a deep discount. That is the definition of exit liquidity testing.

The most powerful counterargument is also simple. Recipients can hold the unlocked tokens, and PUMP is connected to a platform that includes real activity, fees, and historical buyback demand.

This transaction has two observable consequences. Either supply meets enough demand to liquidate without lasting damage, or the market reprices PUMP because available bids are thinner than insider supply.

Timing is important for traders. With cliff vesting, supply decisions that can unfold over months are compressed into a single window, so price movements around a date are live signals of confidence, depth, and whether holders want cash or exposure.

Retail demand for Pump Fun has already been tested once

The tension is even more acute because Pump.fun’s token already had one great demand event. CryptoSlate reported in July 2025 that Memecoin Launchpad sold 150 billion PUMP tokens to retail investors, raising $600 million in 12 minutes, bringing total token sale proceeds to $1.32 billion.

This was the primary market demand under launch conditions. The Cliffs of July 12th is an attempt at something different. The question is whether secondary market liquidity can absorb the supply once trades become stale, the token falls well below its peak, and insiders gain new avenues to liquidity.

The platform situation makes it harder to miss a reversal. Pump.fun has built a reputation for quickly creating and trading meme tokens.

CryptoSlate’s Launchpad review describes CryptoSlate as a Solana-native bonding curve launchpad, where regular users can typically buy and sell immediately, and where the practical constraint is liquidity rather than formal vesting.

In other words, Pump.fun turned the flow of high-velocity retail into a product.

Here, PUMP needs to demonstrate that the same market reflection exists for its own token when the seller profile changes. In the past, retail buyers funded token sales with extraordinary speed.

The next question is whether secondary traders are willing to provide sufficient depth when the expected supply comes from teams and investor categories rather than new public demand.

The problem is not the moral judgment regarding meme coins, but the market structure. PUMP may remain a tradable revenue-linked token, but may still face pressure from cliff vesting.

We may also experience volatility in the short term unless the business proves insolvent. Importantly, the July 12th date turns abstract dilution risk into a measurable trade.

That’s where Pump.fun’s own design history adds to the story. Launchpad has trained users to expect instant market access and quick exit. Unlocking PUMP asks if the platform token depth is the same when the flow moves in the opposite direction.

While the platform has created liquid attention for thousands of tokens, insider supply will test whether the attention is durable enough to support its own market.

PUMP’s share buyback is the basis for absorption

The strongest argument for absorption lies in Pump.fun’s earnings and repurchase history. Tokenomist’s Digest notes that Pump.fun is a stable source of revenue, has implemented token buybacks in the past, and could absorb increased supply if the program is large enough.

CryptoSlate previously investigated that question in the broader token buyback market, noting that as of January 6th, Pump.fun had spent $233 million buying 62.2 billion PUMP.

The same buyback analysis warned that a buyback program would only change the supply landscape if fee income grows faster than planned unlocks.

Here are the filters related to the July 12th cliff. A headline about share buybacks is not enough.

What matters is the scope. That is, how much demand the program is creating for the newly available supply, and whether that demand is visible when insiders are allowed to sell.

If PUMP volume rises to unlock, price holds, and repurchase demand is evident, the market can interpret this event as manageable dilution.

This result leaves future vesting risk, but indicates a higher bid for the token than the headline unlock suggests.

If price weakens while volume increases, the signal changes. High turnover can mean absorption, but it can also mean distribution.

The difference is whether the buyer accepts the supply without forcing a continued discount. Therefore, the price trend after unlocking is more important than the unlocking calendar itself.

If the background is wide, it will feel more oppressive. Tokenomist Weekly Digest explained that June was a defensive period, with Bitcoin falling below $60,000 at the end of the month, creating a headwind for spot Bitcoin ETF flows.

He also said that capital has become selective, favoring tokens with clearer return and value generation mechanisms over the broader market. This is a complex configuration for PUMP. Although the project has revenue, the token has a major insider cliff.

Judgment will be handed down after July 12th

Before unlocking, the most obvious conclusion is conditional. Pump.fun’s July 12 cliff is large enough, concentrated enough, and close enough to recent visible daily volume to qualify as PUMP’s first real exit liquidity test.

Sell-through still doesn’t exist as a variable.

The next signal comes from how PUMP will trade once the token becomes available.

A constructive outcome would be that volumes increase without continued price declines, there is limited evidence of exchange-bound supply, and there is sufficient demand and repurchase activity to maintain market order.

Weak results indicate high volumes combined with price deterioration, suggesting that liquidity is being used for exit rather than accumulation.

Therefore, July 12th is the deadline, and the impact after that is visible. Pump.fun has built one of the fastest retail attention machines in cryptocurrencies.

PUMP must now show whether it has enough attention to meet insider supply when the cliff arrives.