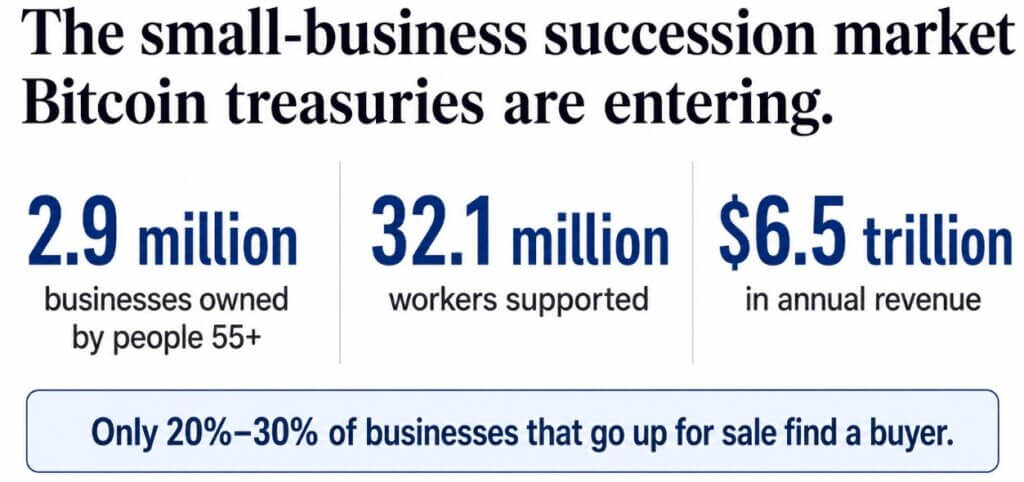

Approximately 2.9 million American businesses are run by people age 55 or older, support 32.1 million workers and generate $6.5 trillion in annual revenue, according to research from Project Equity and Harvard Business School.

According to the Exit Planning Institute, only about 20 to 30 percent of companies put up for sale find a buyer.

Orange Juice Holdings wants to be one of those buyers, with additional plans to buy and permanently hold cash-flow companies that generate $1 million to $10 million a year, pay the sellers some in Orange Juice stock, and put some of the surplus into Bitcoin.

Orange Juice is a newly formed Connecticut permanent capital holding company. It was founded by Ego Death Capital partners Jeff Booth, Lynn Alden, Nico Lechuga, Andy Pitt and Adrian Steckel, with day-to-day operations run by Ruben Zweiban. Mexican billionaire Ricardo Salinas joined as an anchor investor.

The company raised $40 million to acquire and permanently own cash-flowing American companies while building a Bitcoin vault.

Another buyer in a transaction that you are familiar with

The Bitcoin financial model that has made companies like Strategy famous operates through public markets.

The company issues stock to raise capital, uses the proceeds to buy Bitcoin, and the stock trades at a premium or discount to the value of the Bitcoin it owns. This entire loop occurs between the company and the open market trader who selects the buyer.

Orange Juice’s version is run by the founders who sell the business, receive part of the payment in cash and Orange Juice stock, and whose operating cash flow funds both future acquisitions and Bitcoin purchases.

Orange Juice plans to use private equity to make acquisitions before going public, but an eventual listing could make the stock more liquid and easier to use as currency for large-scale acquisitions. Going public remains a goal, but the timing has not yet been set.

If a retired plumbing company owner or local manufacturer accepts orange juice stock as part of their dividends, they may be taking on the same risk as a condition of selling the business they spent decades building.

If they accept shares, they will own a minority stake in a holding company built out of businesses chosen by someone else, run by executives who answer to someone else’s opinions, and, above all, subject to Bitcoin price fluctuations.

Orange Juice documents list a future public listing as a goal the company is working toward, meaning the seller’s stock currently functions purely as debt in the private company.

Concentrated ownership in a business built by the founders after accepting Orange Juice stock prior to sale Minority ownership in a holding company established by others Control of management, capital allocation, and timing Exposure to decisions made by Orange Juice’s management Common operating risks in one company or region Acquisition Operating reorganization across the business Wealth tied to Orange Juice Valuation, Future Liquidity, and Bitcoin Exposure Wealth tied to Suk’s Diversified Business Cash Flow and Sale Value Sale Price is typically negotiated with cash or debt consideration Partial dividends may depend on private equity that is not yet publicly liquid Succession Risks: The post-sale risk of finding the right buyer: whether the buyer’s broader flywheel works.

Flywheel and places where it can break

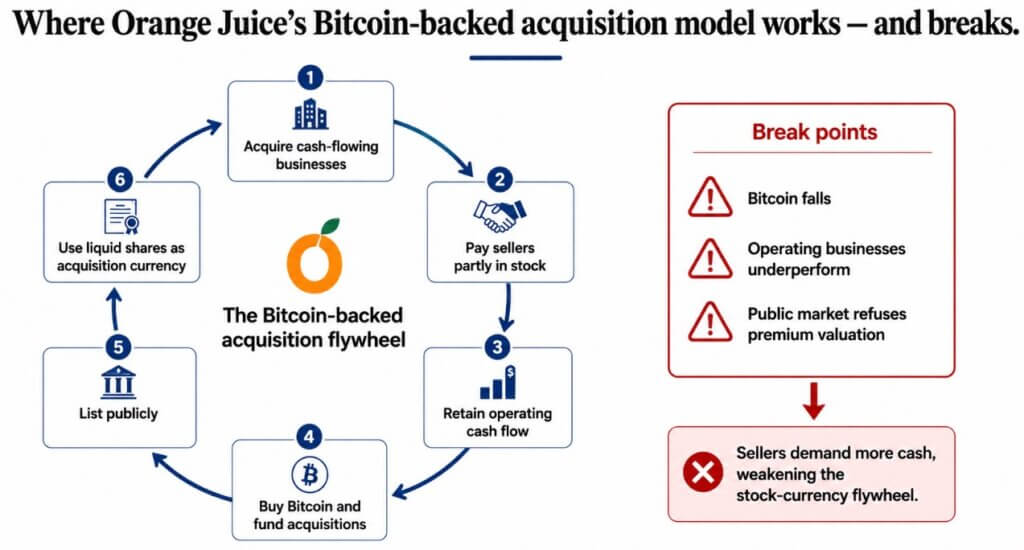

The mechanism involves acquiring a company with cash flow, paying a portion of the stock price, retaining the cash flow to fund further acquisitions and Bitcoin purchases, building a treasury, going public, and using the newly liquid stock to buy the next round of companies.

If Bitcoin falls, if the acquired business underperforms, or if the public market refuses to overvalue the company when it goes public, the seller’s stock becomes significantly less attractive.

Under these circumstances, it becomes difficult to maintain a flywheel built around stocks as a currency.

Galaxy described the standard Bitcoin treasury strategy as a premium-to-NAV loop where a company trades above the value of its Bitcoin holdings, raises equity at that premium, buys more Bitcoin, and uses the resulting story to maintain the premium.

Galaxy also warned that the loop becomes dangerous when the premium disappears because issuing shares close to net asset value will stop adding value and start diluting value.

Many digital asset treasury firms have already hit that wall, trading below their net asset value as token prices fall, and Strategy itself has sold around $218 million in Bitcoin this year to raise dividends and rebuild dollar reserves.

Orange Juice’s business operations provide a unique source of cash flow among treasury-type companies. The acquisition currency portion of the plan remains dependent on the same type of open market valuation that currently burdens other parts of the category.

Two ways the model is executed

If Orange Juice’s operating business does well and the company ends up being valued highly when it goes public on the public markets, sellers will have the confidence to accept more stock and less cash in each transaction.

Then the companies buying the stock, the companies funding Bitcoin and further acquisitions, and the expanding Treasury will in turn support the value of the stock, and the flywheel will work as designed.

If Bitcoin falls or the market becomes skeptical of an eventual listing, sellers will start demanding more cash and less inventory, and the acquired currency portion of the model will stall.

Orange Juice can acquire companies at just higher all-cash costs, which this model was built to avoid.

Orange Juice is testing whether retiring founders would accept a portion of Bitcoin-related equity as part of the consideration for handing over the business they built, and whether enough founders would say yes to make the model work.