Asian Bitcoin company BitPlanet is converting its Bitcoin vault from a balance sheet position to a source of mined BTC revenue.

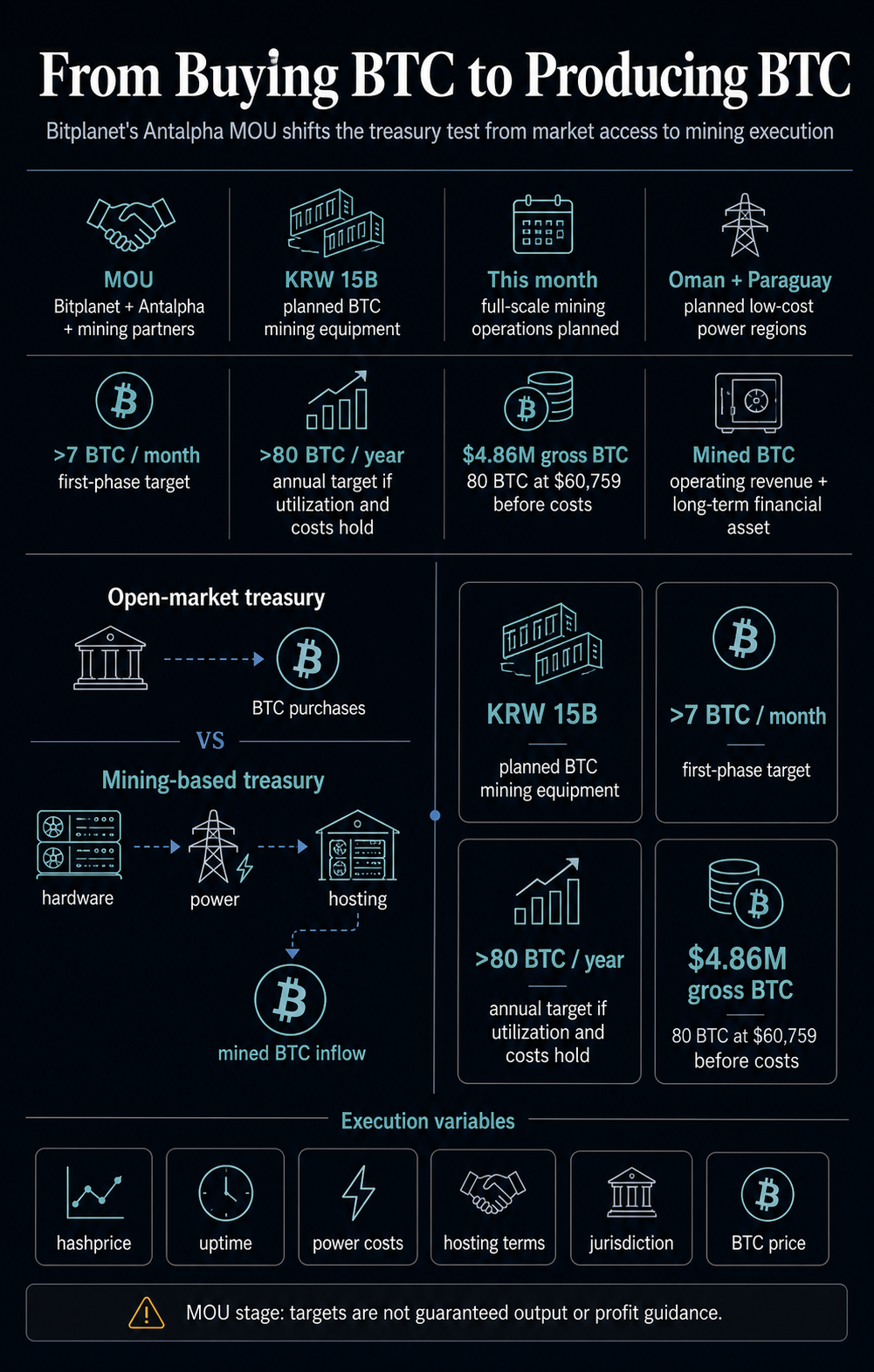

The Korean company announced in a June 24 release that it has signed a strategic memorandum of understanding with Nasdaq-listed Antalfa and mining ecosystem partners.

Based on this MOU, BitPlanet will invest 15 billion won in BTC mining equipment and plan to start full-scale mining operations this month.

This change takes BitPlanet beyond the well-known corporate finance strategy of raising capital, buying BTC, and having balance sheet exposure.

Mining-based treasuries are exposed to a variety of operational stacks, including hashrate, hosting contracts, power prices, equipment uptime, local execution, and whether mined coins are held, sold, or pledged as collateral.

BitPlanet is presenting its second model as the next step in the company’s Bitcoin strategy. The company said that mined BTC will be recognized as operating income and managed as long-term financial assets across liquidity reserves, risk hedge funds, and reinvestment funds.

Financial strategy in full swing

BitPlanet’s announcement expands on the company’s previous financial accumulation. CryptoSlate previously covered Bitplanet’s acquisition of SGA and the company’s ambitions to become one of the largest corporate Bitcoin holders, and later covered the company’s daily Bitcoin accumulation drive.

The previous model was well known. The idea was to raise capital, buy BTC, and reflect the Bitcoin exposure on the balance sheet.

The Antalfa agreement raises other questions. Can treasury companies build iterative Bitcoin production loops where hardware, low-cost power, and hosting infrastructure feed coins to their balance sheets over time?

According to BitPlanet, the first stage of equipment is expected to generate over 7 BTC per month and 80 BTC per year, depending on equipment utilization and electricity costs.

Using a Bitcoin price of around $61,000, 80 BTC equates to approximately $4.9 million in total BTC production, excluding power, hosting, financing, repairs, taxes, and corporate overhead.

This calculation provides investors with a measure of scale rather than a guide to profit. Also left open is whether the company can retain, reinvest, or use the mined BTC as collateral without undermining its broader financial thesis.

What adds to the model BTCKey DependenciesKey RisksPublic Market Financial AccumulationPurchases with cash, equity, debt, and other financingCapital Market Access and BTC Price Dilution, Debt Costs, or Forced Stops of PurchasesMining-based BTC InflowsASIC Equipment, Hosting, Power, and OperationsRunning Hash Prices, Uptime, Power Conditions, DeploymentQuality Mining Margin Compression or Decrease in Coin Retention

Antalpha is more than just a name in this announcement. The company has priced its IPO in May 2025 and trades on the Nasdaq under ANTA.

Its public documents describe businesses built around Bitcoin mining finance, including mining machine loans, hash rate loans, supply chain credits, and margin lending services through Antalpha Prime.

Antalfa’s IPO prospectus described financing products related to rigs, hosting, maintenance, and mine operating costs. Antalpha Prime’s documentation adds operational links and describes funding arrangements where mined BTC can be used as collateral for hosting, repairs, and other service costs.

This creates operational challenges for BitPlanet, as mining is capital intensive before producing anything. Equipment must be purchased or financed, shipped, installed, hosted, powered, maintained, and connected to the network.

When a treasury company announces its goals in Bitcoin terms, the real test is whether its operational stack can produce coins at a cost below the value BitPlanet assigns to holding the coins.

Antalfa’s own results constrain that story. The company reported that total facilitated financing in Q1 2026 decreased 3% year over year, despite a 52% increase in revenue, and supply chain TVL decreased by 25%.

As such, the BitPlanet MOU is a test of execution within a still cash-rich lending market.

Planned electricity markets come with risks

According to BitPlanet, the equipment is expected to be introduced in overseas regions where electricity rates are competitive and the electricity environment is stable, such as Oman and Paraguay.

He also explained an overseas colocation model that combines outsourced work and joint ventures.

This structure is central to theory and risk. Mining margins can be won or lost depending on power conditions, reduction risk, hosting reliability, repair time, and the percentage of mined BTC that the company ends up covering its costs.

Deploying into low-cost electricity markets makes sense on paper, but only if the contracts, operating hours, tariffs, taxes, and trading partners can bear it in practice.

The current mining context requires its scrutiny. The Hash Rate Index recently showed the Bitcoin hash price at approximately $30.72 per PH per day.

In a review for May 2026, he noted that the hash price averaged $36.60, but as the difficulty level increased, it dropped to $33.58 at the end of the month.

VanEck’s Bitcoin ChainCheck in mid-June estimated miner revenue in May 2026 to be around $1.12 billion, down 26% year-over-year, noting that miners are selling BTC and moving to AI and high-performance computing.

BitPlanet enters mining as public market investors are already trying to differentiate between companies that own BTC, those that can produce BTC, and those that can convert power infrastructure into another source of revenue.

Recent coverage of miner AI infrastructure by CryptoSlate shows how quickly markets can reprice power assets before they are fully operational.

So mining changes what investors have to measure. The question shifts from how much BTC BitPlanet can buy to whether it can operate, fund, and hold the BTC it mines through a full cost cycle.

These variables make BitPlanet’s next disclosure more important than headline production goals, as economics are determined by contracts, machine performance, and coin retention after costs.

The test for investors is the retention of the coin

The timing is also more stressful for Bitcoin treasury companies.

CryptoSlate recently analyzed how Strategy’s STRC pressure could force trade-offs between cash, BTC purchases, and dilution.

The same broad tensions apply across sectors. Financial strategies that rely primarily on external capital will find it difficult to scale as financing conditions worsen.

Mining provides possible answers with clear trade-offs. If BitPlanet can mine BTC at an attractive cost and hold enough Bitcoin, the company could supplement its purchases with organic coin production.

If hash prices drop, power costs rise, uptime is disappointing, or hosting conditions absorb too much production, the same mining program can become a new capital-intensive burden.

Comparisons with operating miners are also grim. CryptoSlate recently reported that Bitdeer mined 921 BTC in May, but the market was still evaluating how much of that production would be converted into stronger holdings.

BitPlanet’s goal of over 80 BTC per year is much smaller, but the same questions apply. Mined coins will only improve the financial model if their value is sufficient to withstand operating costs and balance sheet demands.

The Korean company’s crypto background adds yet another layer. The Financial Services Commission has in principle restricted corporate crypto asset trading since 2017, and announced in 2025 that it would be gradually reintroduced.

BitPlanet is therefore testing how Korean listed companies can combine their Bitcoin financial strategy, operating revenue, and overseas infrastructure without changing their model to a simple BTC buying agency.

The following signals are evidence of adoption. Signed hosting or joint venture terms, equipment hashrate, power cost disclosure, monthly BTC production, and the amount of mined BTC that remains on BitPlanet’s balance sheet excluding expenses.