SpaceX shares rose in early market trading on Monday, extending gains from a record IPO debut after Elon Musk said the company’s annual revenue could reach $1 trillion by the end of 2020.

The company’s shares are trading around $170, up about 6% from Friday’s closing price, according to Yahoo Finance data.

The move follows a strong first session in which SpaceX priced its initial public offering at $135 per share, opening at $150 and closing at $161.11, giving the company a market value of approximately $2.2 trillion.

This increase also spread to crypto-related derivatives linked to stock prices. SpaceX futures trading volume rose 140% to nearly $930 million, with open interest exceeding $540 million, according to CoinGlass data.

The early market launch added new momentum to one of the hottest public stocks in recent years, underscoring investors’ appetite for exposure to Musk’s rocket, satellite and artificial intelligence companies following the biggest IPO in history.

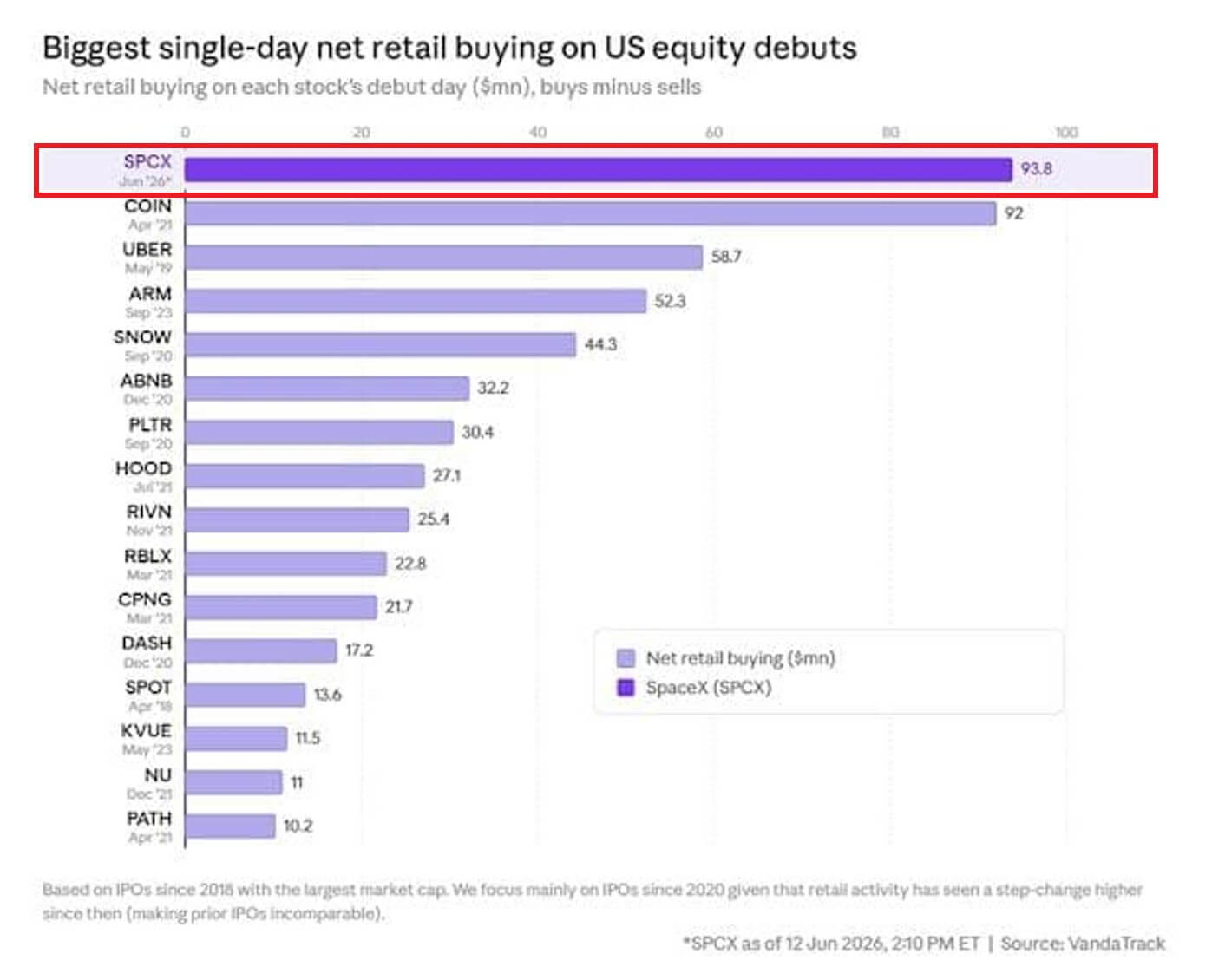

Retail drives SpaceX’s record IPO debut

SpaceX raised $75 billion on its first day of trading, making it the largest IPO in history and quickly making the rocket, satellite and artificial intelligence company one of the most valuable publicly traded companies in the United States.

The company has a market value of more than $2 trillion, second only to Amazon at $2.54 trillion and ahead of Broadcom at $1.81 trillion.

Available data shows that retail investors played a central role in its debut.

Retail investors net-bought $93.8 million in SpaceX stock on Friday, the largest single-day net retail purchase for an IPO, according to data from Vanda Research.

Additionally, SpaceX accounted for approximately 4% of all single-stock retail sales on the day, with net purchases more than 3.5 times larger than the next most purchased stock, Nvidia.

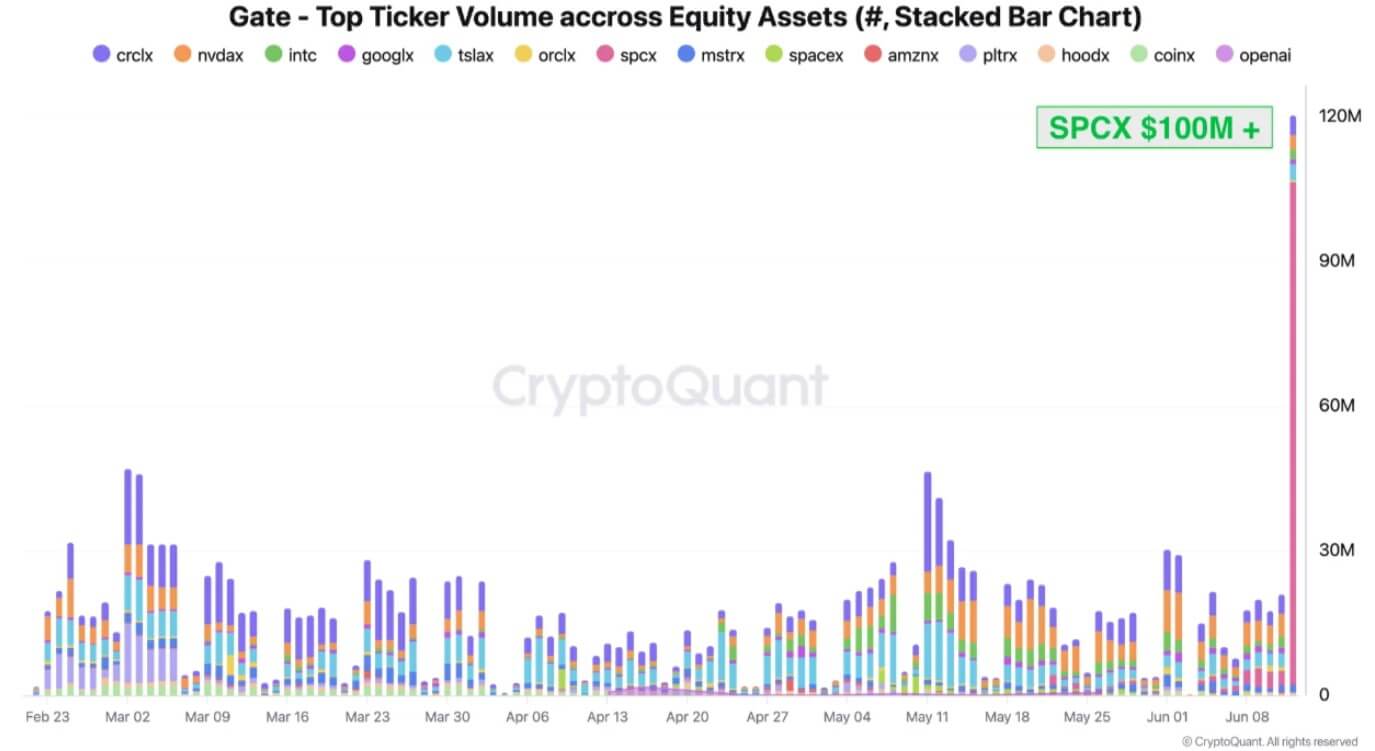

Meanwhile, the listing also spilled over into the crypto market, with traders using tokenized equity products and derivatives to gain exposure to the stock. This is especially noticeableConsidering the challenges that marked the first trading days on some cryptocurrency trading platforms such as Binance.

Still, CryptoQuant’s data showed strong activity across platforms that listed equipment linked to SpaceX. On Gate.com, the trading volume of the tokenized SPCX ticker exceeded $100 million on the first day. By comparison, Circle’s trading volume at the same venue was approximately $4 million, and Tesla’s trading volume was approximately $3.5 million.

Stock-linked tokens on Gate.com typically generate between $10 million and $25 million in volume per day across assets as shown in the platform’s data. SpaceX’s first day activity was well above that range, demonstrating the scale of demand among crypto-native traders.

This activity suggests that tokenized stocks are becoming a more visible vehicle for major stock market events. These products remain small compared to traditional stock markets, and their regulatory treatment varies by jurisdiction.

Still, SpaceX’s debut showed that crypto traders are willing to use on-chain or exchange-based means to gain exposure to high-profile public companies without leaving the digital asset arena.

Musk expands the growth case

SpaceX’s bull run gained further momentum over the weekend when Musk posted on X that the company could generate $1 trillion in annual revenue by 2030. He added that he would be surprised if the company could not surpass that level by 2031.

The forecast gave investors a new benchmark for a stock already trading at one of the highest valuations on the public market. SpaceX reported revenue of about $18.7 billion in 2025, meaning Musk’s goal would require a more than 50-fold increase in revenue in about five years.

This forecast is well ahead of some of Wall Street’s most optimistic forecasts. Morgan Stanley predicts revenue of about $330 billion by 2030, which means Musk’s number is about three times that forecast.

Meanwhile, Brett Winton, chief futurist at Ark Invest, took a more positive long-term view, saying Starlink and StarShield could generate more than $1 trillion in excess cash by 2035, with annual profits reaching $400 billion.

The large gap between current earnings and these projections helps explain the debate surrounding SpaceX’s valuation.

Although the company’s revenue base is large for an aerospace business, it is still small compared to the current stock market value. Revenues in 2025 recorded significant year-over-year growth, with revenue in the first quarter of 2026 being approximately $4.69 billion.

However, the company remained in the red due to increased expenses.

This means investors backing this stock are betting that multiple businesses can grow at the same time. SpaceX’s satellite broadband network, Starlink, is the company’s biggest near-term revenue driver. This will be a meaningful source of recurring revenue and provide SpaceX with global consumer and enterprise products beyond traditional launch services.

StarShield, the government-focused satellite communications sector, is also part of the bull case as demand for secure connectivity increases among defense and public sector customers.

Starship has a more speculative upside aspect. This launch system is designed to reduce the cost of reaching orbit and support larger commercial, government, and scientific missions. SpaceX is positioning it as a core for future markets in space logistics, lunar operations, Mars exploration, and other forms of transportation.

The company is also expanding its efforts into areas related to artificial intelligence, telecommunications, and space infrastructure.

Its prospectus pegs the total market that could realize these ambitions at up to $28.5 trillion, a figure that includes several industries that are still in the early stages of development.

These forecasts help explain the intensity of demand before and after an IPO. It also shows how much SpaceX’s valuation depends on a company that needs to scale quickly, absorb large investments and avoid major technological or regulatory setbacks.

Intense scrutiny surrounding SpaceX’s reputation emerges

Meanwhile, SpaceX’s market momentum has drawn warning from analysts, who say the company’s valuation leaves little room for slower growth, higher costs and delays in major projects.

CFRA analysts cited SpaceX’s challenging growth expectations, high valuation and significant capital needs as the main reasons for their cautious view.

Those costs are already rising. SpaceX reported capital expenditures of $10.1 billion for the three months ended March, compared with $4.1 billion in the year-ago period. This increase reflects spending on artificial intelligence infrastructure, Starship development, and other long-term projects.

At the same time, profitability remains another pressure point. The company will lose nearly $5 billion in 2025, with cumulative losses over the past few years estimated at $50 billion.

SpaceX also warned in its prospectus that it may never turn a profit, and the disclosure underscores how much more it still needs to spend before its biggest bet matures.

Henrik Seberg, a macro analyst at SwissBlock, said that despite the losses, the market is treating SpaceX as one of the most valuable companies in the world.

He compared this valuation to past periods of market overperformance and argued that investors are paying upfront for the company’s unproven earning power.

According to him:

“Make no mistake about it. We have the biggest bubble in history and it will burst. Not yet. Expect us to soar to the final top…but soon!”

Nevertheless, Wall Street’s initial targets show little agreement on where stocks should trade.

Loop Capital’s highest price target is $349, followed by Baird at $320 and Bernstein at $310. Oppenheimer set a target of $190, and New Street Research set a target of $165.

Although the average is around $267, the wide range reflects widely differing views about SpaceX’s future revenues, profits, and market opportunities.

To sustain the bull market, SpaceX will need to show that its biggest business can grow fast enough to support the price investors are paying. The market will be watching for updates on Starlink’s growth, Starship’s progress, government contracts, AI spending, and any signs of revenue approaching Musk’s $1 trillion goal.

For now, investors are paying a premium for access to companies that have been out of reach on the public markets for years. That premium could remain if SpaceX continues to expand rapidly, but the stock would remain at risk if costs rise faster than expected or if the path to profitability takes longer than the market currently assumes.