Arthur Hayes outlined a path to a Bitcoin price of $1 million built around liquidity absorption by AI, debt collapse, printing by authorities, and capital rotation into cryptocurrencies.

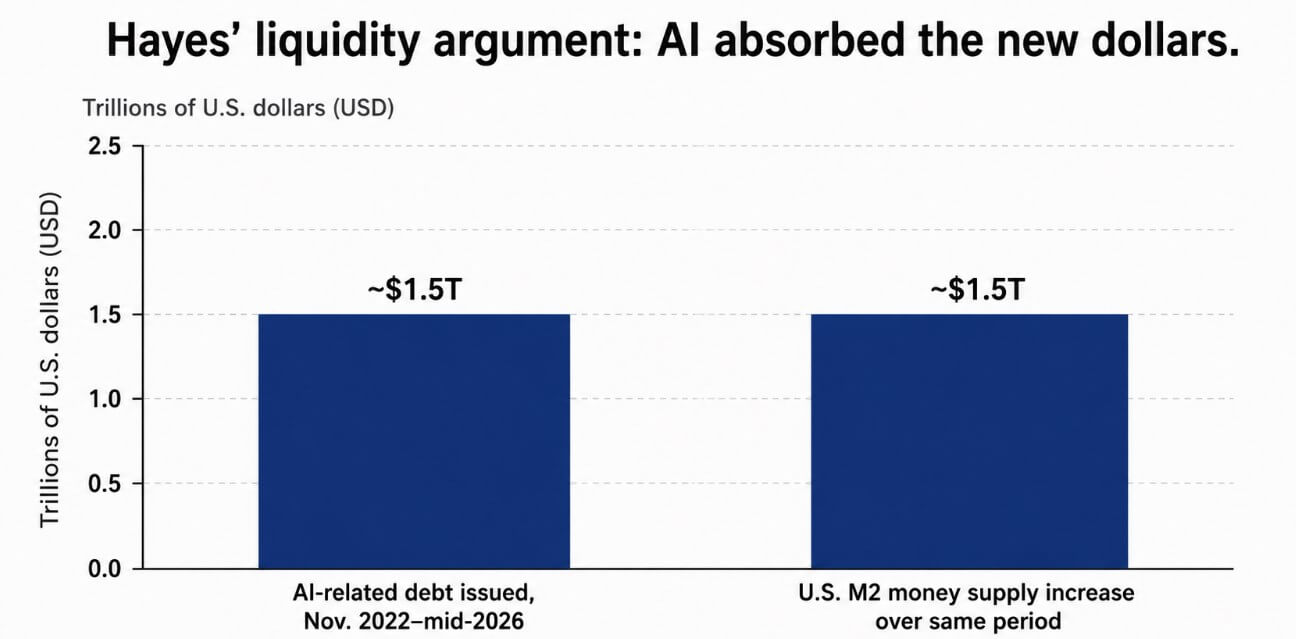

Regarding bankless, Hayes argued that AI has become a major capital sink, noting in his Substack essay that approximately $1.5 trillion of AI-related bonds were issued between November 2022 and mid-2026.

This amount roughly matches the $1.5 trillion increase in M2 money supply over the same period, with the newly created dollars absorbed into data centers and GPU clusters before they could reach Bitcoin’s bid.

Luke Gromen, founder of Forest for the Trees, arrived at the same diagnosis through a different gateway. Speaking on the Coin Stories podcast in June, he said the current market structure is unhealthy under record stock indexes, with profits concentrated in AI stocks and narrowing in breadth.

Gromen said:

“AI is sucking all the oxygen, all the liquidity out of the room. I think that’s happening with Bitcoin as well.”

He described Bitcoin as “one of the last working alarm bells on liquidity,” a signal asset that alerts investors to the overall picture of liquidity before other markets confirm it.

Gromen sold most of his Bitcoin position near its all-time high and only slowly returned it, which is consistent with Hayes’ short-term bearish stance on the cryptocurrency.

He extends the discussion to AI infrastructure accounting, where companies prepay revenue while spreading construction costs over time, inflating reported profits and masking moments when a slowdown in construction forces a sharp slowdown in cash flow.

Serious macro institutions are also concerned about Bitcoin price

Torsten Slok, chief economist at Apollo, wrote that the top 10 companies in the S&P 500 are more overvalued than the top 10 during the tech bubble of the 1990s.

These 10 stocks currently make up about 40% of the index, and when you invest $100 in the S&P 500, you’re betting that the AI story will continue. The broad adjustments in this group extend to all passive portfolios worldwide.

The Bank for International Settlements has published a 2026 report documenting Hayes’ explanation, but there is central bank credibility behind this warning. BIS found that investments in AI infrastructure are shifting from internal cash flow to external debt as the scale of investment required overwhelms hyperscalers’ free cash flow.

Private credit outstanding to AI-related companies increased from almost nothing to more than $200 billion, and their share of total private credit rose from less than 1% to nearly 8%.

The BIS has warned of risks to credit standards and financial stability if expected returns fall short, and found that hyperscalers are also taking AI infrastructure debt off their balance sheets through special purpose vehicles and operating leases, which the BIS calls “shadow borrowing.”

These moves would strengthen the ties between tech companies and non-bank investors, creating new channels for shocks to be transmitted if sentiment reverses.

With more than $200 billion of private credit built up in AI infrastructure with maturities of five to seven years, AI slowdown becomes a credit market risk rather than a narrow technology issue.

Evidence in the Risk Layer ArticleWhy it matters to Bitcoin price theoryLiquidity drainHayes and Gromen claim AI absorbs capital that might have otherwise supported Bitcoin priceExplains why BTC lags behind despite expansion in money supplyStock concentrationApollo on top of S&P 500 Top 10 stocks say they are more overvalued than during the 1990s tech bubble. Mega-cap revisions heavy on AI will hurt passive portfolios Globally debt-financed BIS says AI infrastructure financing is shifting from internal cash flow to external debt Private credit exposure turns AI from tech stock story to credit market story BIS says AI-related private credit has increased from nearly zero to more than $200 Create non-bank remittance channels if BCAI delivers disappointing results Shadow borrowing BIS flags SPVs and operating leases used to finance infrastructure off-balance sheet Policies that obscure the true leverage behind AI Hayes claims that if it collapses, authorities will be forced to print Bitcoin price rise depends on bailout liquidity seeking scarce assets

Where macro opinions differ

Lynn Alden’s framework provides a financial background for Hayes and stops at a less dramatic conclusion.

In her February and March newsletters, Ms. Alden explained that the Fed will enter into what she calls a “step print” in which its balance sheet expands in line with nominal GDP growth, in a range of $220 billion to $375 billion in 2026, far below the scale of previous crisis quantitative easing.

Her standard for calling it a true blockbuster is $2 trillion or more. Hayes describes a future crisis response that clears that hurdle, while Alden describes the current base case of about $300 billion.

Bitwise’s 2026 Advisor Study found that of the 299 financial advisors surveyed, 32% of their client accounts will be allocated to cryptocurrencies in 2025, the highest percentage in the study’s eight-year history.

Among crypto themes tracked, “digital gold” and the decline in the value of fiat currencies ranked second at 22%, behind stablecoins and tokenization at 30%. Stories of Depravity are already distributed through ETFs and incorporated into the portfolios of professionals.

If the Fed’s response becomes a market topic, Bitcoin already has institutional arguments built into its existing allocations.

order problem

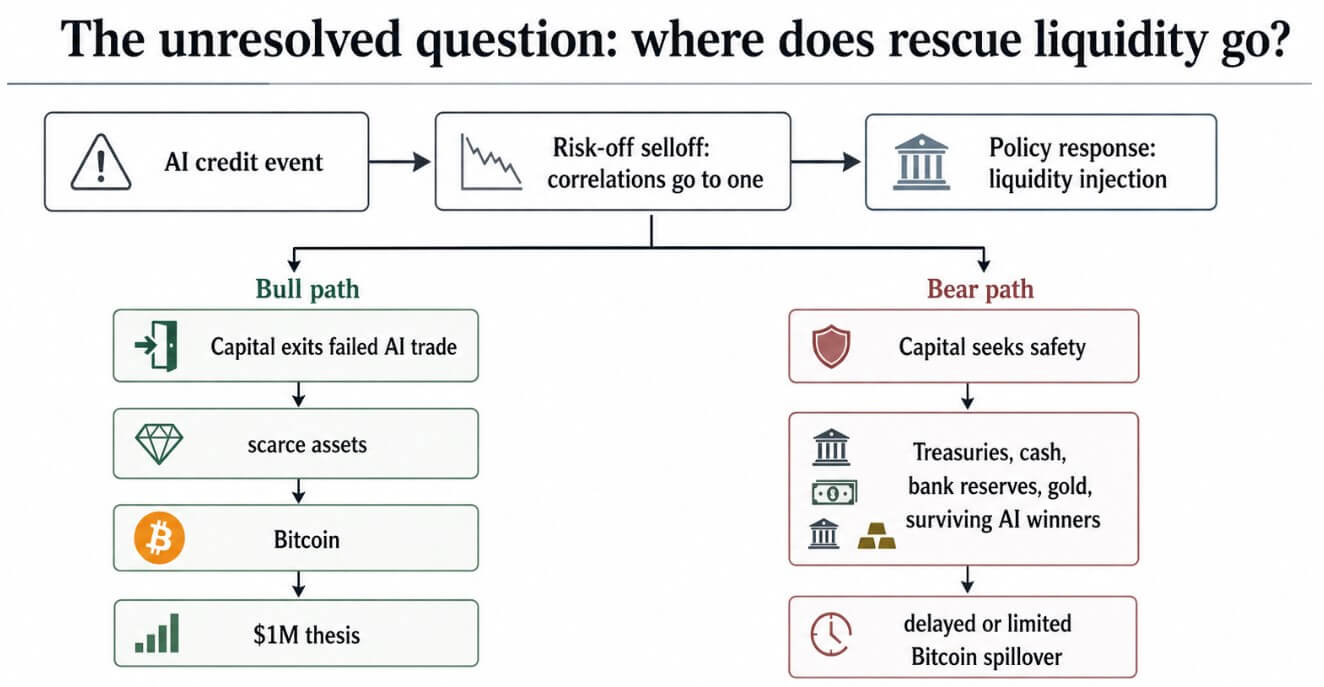

Hayes acknowledged on Bankless that in a broad risk-off event, correlations compress to one and investors sell everything.

Despite the expansion in the money supply, the price of Bitcoin has fallen by about 50% from its October 2025 high of $126,000.

AI trust events will also trigger a similar first-stage response. Before policymakers can react, Bitcoin is sold off along with risky assets, banks hold back on lending, and liquidity tightens.

The real deal for Hayes is the policy response after the crash, and whether investors who have seen AI destroy their capital will put their newly printed money back into the same sectors.

Liquidity drain analysis, BIS debt data, and Apollo Rating alerts document that setup. The destination of capital is determined within the crisis itself, and their sources cease during a crisis.

Two ways money affects the price of Bitcoin

For bulls, the entire haze sequence depends on them arriving unscathed. AI financing stress hits banks and private credit, policymakers inject massive liquidity, and investors who saw $1.5 trillion of AI debt destroy value are seeking scarce assets unbundled from failed deals.

A Bitcoin price of $1 million per coin would imply a fully diluted network value of approximately $21 trillion, a figure that would require a massive reallocation of crypto-native capital and global macro portfolios.

Alden’s graduated printing environment supports directionality. Only the injection of Hayes’ scale of crisis creates its scale.

The bearish case is that emergency liquidity goes first to the safest collateral, such as government bonds, cash, bank reserves, and gold. The surviving AI winners will raise money from investors seeking the most powerful projects in the space and keep their money within the technology.

Bitcoin’s correlation with risk assets in the early stages of a credit event defeats Hayes’ purpose, and bailout funds could remain in U.S. Treasuries, gold, and bank reserves for months before reaching cryptocurrencies.

Hayes’ settings regarding AI debt, overvaluation, and liquidity distortions may prove to be entirely accurate. His destination depends, in part, on investor behavior during the crisis, but that part remains unresolved.