While Circle’s $222 million ARC token presale gave Wall Street a new way to value USDC issuers, it also raised more difficult questions for one of crypto’s most profitable partnerships.

Circle announced on May 11 that investors led by a16z Crypto have supported the presale of ARC, the native token of Arc, the company’s planned public blockchain for institutional finance.

The sale values the network at $3 billion on a fully diluted basis, and was announced in conjunction with first-quarter results in which total revenue and reserve income increased 20% year-over-year to $694 million.

At the same time, USDC’s circulation amount increased by 28% to $77 billion, and on-chain transaction volume reached $21.5 trillion, an increase of 263% year-on-year.

These numbers strengthened Circle’s position as one of the leading issuers in the global stablecoin market, where tokenized dollars have become the core infrastructure for trading, payments and settlements.

But the more important development is that Circle has moved beyond issuance through its new blockchain network, Arc.

Arc provides the company with a network-level growth story built around payments, tokenized assets, foreign exchange, capital markets, and AI-driven commerce.

This brings Circle closer to territory already occupied by Coinbase, a longtime USDC partner and operator of Base, a layer-2 network that the U.S.-based exchange positions as a clearing layer for stablecoins, consumer payments, and proxy transactions.

Considering this, Circle’s aggressive expansion could bring new competition to the crypto industry, namely an impending head-to-head showdown with Coinbase.

Circle offers investors a wide range of stories

Circle’s business has long been tied to the economics of stablecoin reserves. The company issues USDC, holds safe-haven assets backing its tokens, and earns income from its reserves.

This model could be powerful if interest rates rise, but it also raises questions about how long returns will persist as interest income declines.

Arc is Circle’s answer to that concern.

The company pitches the network as the Internet’s “economic operating system,” a shared environment where stablecoins, tokenized assets, and financial applications can run on a common infrastructure.

The chain is expected to be EVM compatible and feature stablecoin-native fees, deterministic sub-second finality, and configurable privacy designed for institutions that require auditability without exposing all transaction details to the public.

Circle CEO Jeremy Allaire structured the quarter around the convergence of AI platforms and on-chain money, stating:

“Circle’s first quarter reflected strong execution on the larger opportunity as AI platforms and economic operating systems rapidly converge on the new Internet stack. With the ARC token presale, Arc network momentum, and agent stack launch, we are building a trusted infrastructure for AI-native economic activity and a more programmable Internet financial system.”

The list of investors shows how far the proposal currently stands. a16z Crypto led the presale with a $75 million investment.

Other participants include BlackRock, Apollo Funds, Intercontinental Exchange, SBI Group, Janus Henderson Investors, Standard Chartered Ventures, General Catalyst, IDG Capital, Haun Ventures, and Bullish.

The message to investors is clear. Circle wants to be valued as a full-stack infrastructure company in on-chain finance, rather than a stablecoin issuer exposed to interest rate cycles.

In a note shared with CryptoSlate, Clear Street analysts echoed that view, writing that Circle is “no longer a pure crypto play” and has built the Layer 1 network, application layer, and partner ecosystem necessary to become a significant infrastructure provider.

The firm raised its price target on the company from $152 to $157, citing Ark, AgentStack, Circle Payments Network, and regulatory momentum as potential upside factors.

Ark provides a unique venue for the circle

Circle’s new Arc blockchain changes the company’s role in the stablecoin economy.

USDC already spans over 30 blockchains and is integrated across exchanges, wallets, fintech platforms, and institutional systems.

This decentralization is one of the main strengths of stablecoins. Regardless of where the movement takes hold, Circle is likely to grow as USDC becomes more widely used.

Arc gives you a reason to bring more of that activity into your Circle-managed infrastructure.

The network is designed to support payments, lending, foreign exchange, capital markets, and tokenized assets. Circle also positions ARC as a coordination token for validators, builders, liquidity providers, exchanges, institutions, and users.

In this structure, USDC remains the trading asset, while ARC is intended to manage economic rules and coordinate network participants.

This creates a broader economic layer around Circle’s core product. If Arc gains traction, investors will no longer be solely evaluating Circle based on USDC circulation and reserve income.

We also track transaction volumes, developer recruitment, institutional participation, validator activity, and the extent to which Circle is able to earn revenue from the infrastructure surrounding USDC.

Circle Payments Network adds another piece to that strategy. According to ClearStreet, CPN’s annual payments totaled $8.3 billion, approaching $10 billion as of May 7, and 136 financial institutions have registered.

Managed payments aim to reduce friction between banks and payment service providers by handling the burden of licensing, liquidity, custody, and compliance.

Together, Arc, Agent Stack, CPN, and managed payments enable Circle to deliver a more ambitious public market story. The company is trying to become the platform where digital dollars move, are settled, and interact with software.

That ambition makes Coinbase’s relationship more complicated.

Coinbase already controls much of the flow

However, Coinbase has its own claims to the USDC infrastructure story.

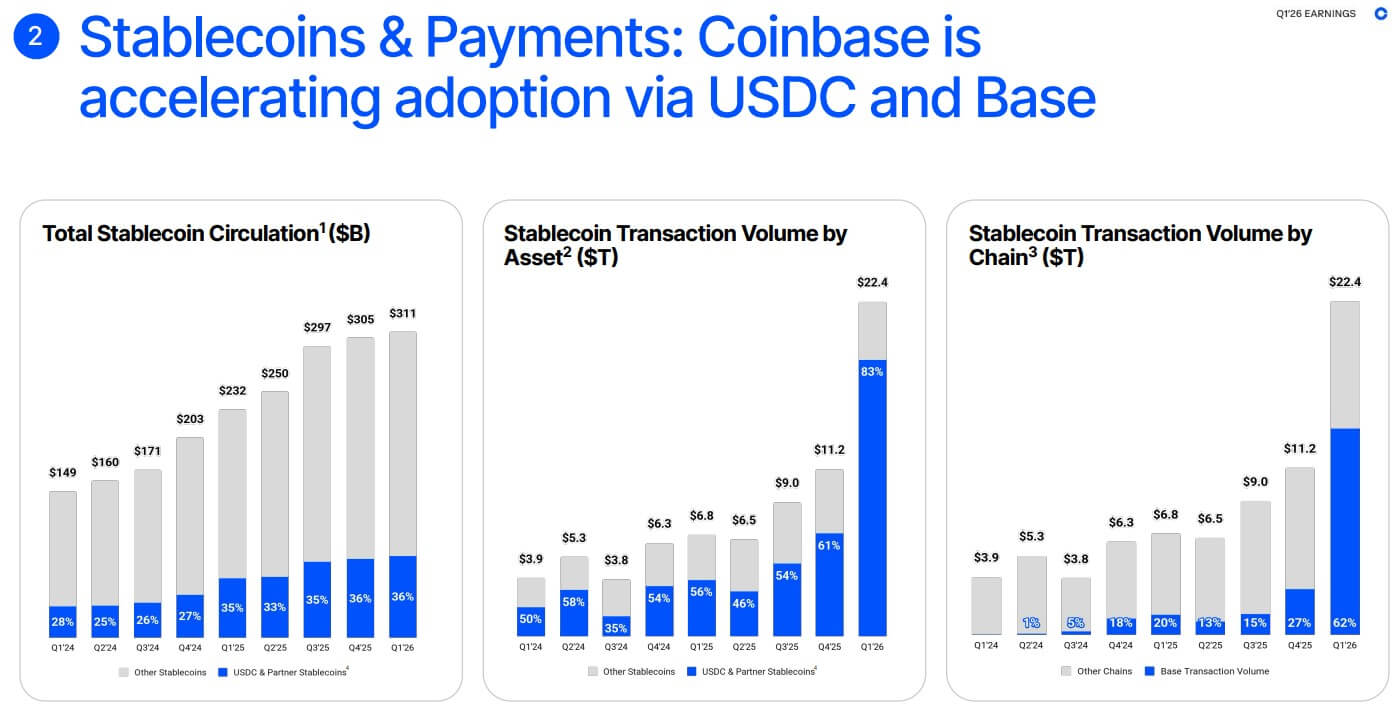

In its first quarter report, the company described itself as a USDC distribution engine, with over 25% of the total USDC in circulation, or an average of over $19 billion, held across Coinbase products.

According to Coinbase, Base processed 62% of the world’s on-chain stablecoin transaction volume in the quarter, more than all other chains combined.

The company also said that over 90% of on-chain agent stablecoin trading volume occurs on Base, making Coinbase the leading platform for agent commerce.

At the same time, over 100 million payments were processed through the x402 protocol, with over 99% completed using USDC.

These numbers show why Arc is sensitive to Coinbase.

Coinbase is no longer just a distribution channel for Circle’s stablecoins. We are building rails around our assets.

Its stack includes USDC as a programmable dollar, Base as a low-cost payments network, and Coinbase Developer Platform, AgentKit, and x402 as infrastructure for developers and AI-enabled payments.

Circle spawn stacks are facing the same direction. USDC provides dollar assets, Arc provides the network, Agent Stack targets AI-native commerce, and CPN connects financial institutions and payment companies.

The two companies continue to collaborate commercially around USDC’s growth. But their infrastructure strategies increasingly point in the same vein.

New scoreboard added to Alliance

For years, Circle and Coinbase’s relationship has been one of crypto’s cleanest partnerships. Circle issued USDC. Coinbase distributed it across its exchanges, wallets, and institutional products. Stablecoins gained scale and Coinbase shared the economics.

This relationship has made USDC one of the most important dollar assets in cryptocurrencies. It also gave Coinbase a major stablecoin revenue stream and helped make USDC a regulated alternative to Tether’s USDT for many US-based institutions.

However, Arc introduces a different incentive structure.

Dragonfly investor OmarKanji captured the concerns in a post asking how long the “marriage” between Circle and Coinbase will last.

His argument was that the old model worked when Circle was the issuer and Coinbase was the seller. But with Circle’s public market demand and Arc’s token-backed network, the company now needs to demonstrate to investors that it can directly own more of its customers, flows, and infrastructure.

That’s where the Arc overlaps the Base. Circle wants Arc to host USDC balances, tokenized assets, payments, settlements, and eventually foreign exchange activity. Coinbase wants Base to serve as the primary venue for stablecoin payments, on-chain consumer transactions, AI agent activities, and institutional payments.

The tension is already evident in adjacent products. Coinbase has cbBTC, a wrapped BTC product used throughout DeFi. Circle is preparing cirBTC, which is designed to integrate with Arc and Circle Mint.

This overlap does not immediately signal a rift, but it does indicate that the two companies are no longer staying in separate lanes and are starting to compete on similar products.

AI payments increase risk

This competition becomes even more important from an agent commerce perspective.

AI agents are expected to account for a larger share of internet activity, handling tasks such as purchasing data, paying for software, settling bills, managing subscriptions, and running business processes.

These transactions require programmable currencies, low-cost payments, and infrastructure that can approve spending without ongoing human intervention.

Stablecoins are ideal for that environment because they operate continuously, settle quickly, and can be built directly into software. That makes agent commerce one of the most attractive long-term stories for stablecoin infrastructure providers.

Coinbase has already claimed early leadership. Its Q1 materials pointed to Base’s share of on-chain agent stablecoin trading volume and rapid growth in x402 payments. The company offers Base, USDC, AgentKit, and x402 as ready-made stacks for machine-driven economic activities.

Circle is moving to meet that opportunity with Agent Stack and Arc. Allaire is assembling its AI platform and on-chain money as part of a new internet stack, and Circle’s product roadmap suggests the company wants to make USDC a payments layer for software agents as well as humans and institutions.

Considering this, Tom Wan, Head of Data at Entropy Research, concluded:

“[Circle and Coinbase’s]business areas are converging across blockchain, tokenization, payments, and stablecoins. A formal split is unlikely given the mutual interests that are still subject to negotiation, but the trajectory is clear. Both sides are building toward a less dependent relationship, and overlap will only create more friction over time.”