Venture capital is the lifeblood of the startup world in Web3 and cryptocurrencies. Entrepreneurs need to finance their projects in order to hire talented people, pay operating costs, and market to expand their business.

Of course, venture capitalists are happy to do this because they get a cut of the long-term profits. Most startups fail and businesses rely heavily on unicorns driving venture funds.

Indeed, the crypto market is unique, and cryptocurrencies also play a role in many startups issuing tokens. However, the digital asset market is not doing so well.

The orange asset has been in the red by 25% since October, when the price per BTC reached an astonishing record level of $126,000.

Cryptocurrency prices are having an impact on the VC market, and the dynamics of how startups raise funds are definitely changing. What is the overall outlook now?

Sponsored Sponsored

“Market cycles can impact investment sentiment and can slow or accelerate the pace of deal closings,” said Stephen Dice, CEO of Hashgraph Group, which focuses on VC in the Hedera ecosystem.

Decreasing expectations from venture capital

One of the first things that happens when cryptocurrencies go into a down cycle is that startup valuations drop.

It may seem unrelated, but the concept of “hot rounds” for fashionable startups has cooled, and venture capitalists aren’t actually looking for such high valuations, notes Artem Gordadze, an angel investor at the NEAR Foundation and an advisor to startup accelerator Techstars.

“When Bitcoin is trading at high levels, like the $100,000 level, startup valuations are commensurately high,” Goldadze said. “This creates a difficult dynamic: VCs must justify their entry valuation based on the potential future price that needs to be realized within the investment horizon to generate an acceptable return.”

The theory that Bitcoin will always rise seems foreign to venture capitalists. VC investments are long-term, so we see many cycles, especially in Bitcoin.

Additionally, many VCs often refer to November and December as “amortization” months. This means they don’t expect to do too much work during the fourth quarter and holiday season, preferring to start investing anew after the calendar turns to the next year.

Sponsored Sponsored

practical view

The 10,000-foot-above venture perspective, especially as it pertains to the crypto sector, is one of spending, but less in volume.

Case in point: Prediction market Polymarket raised $1 billion and Kraken raised $800 million this quarter.

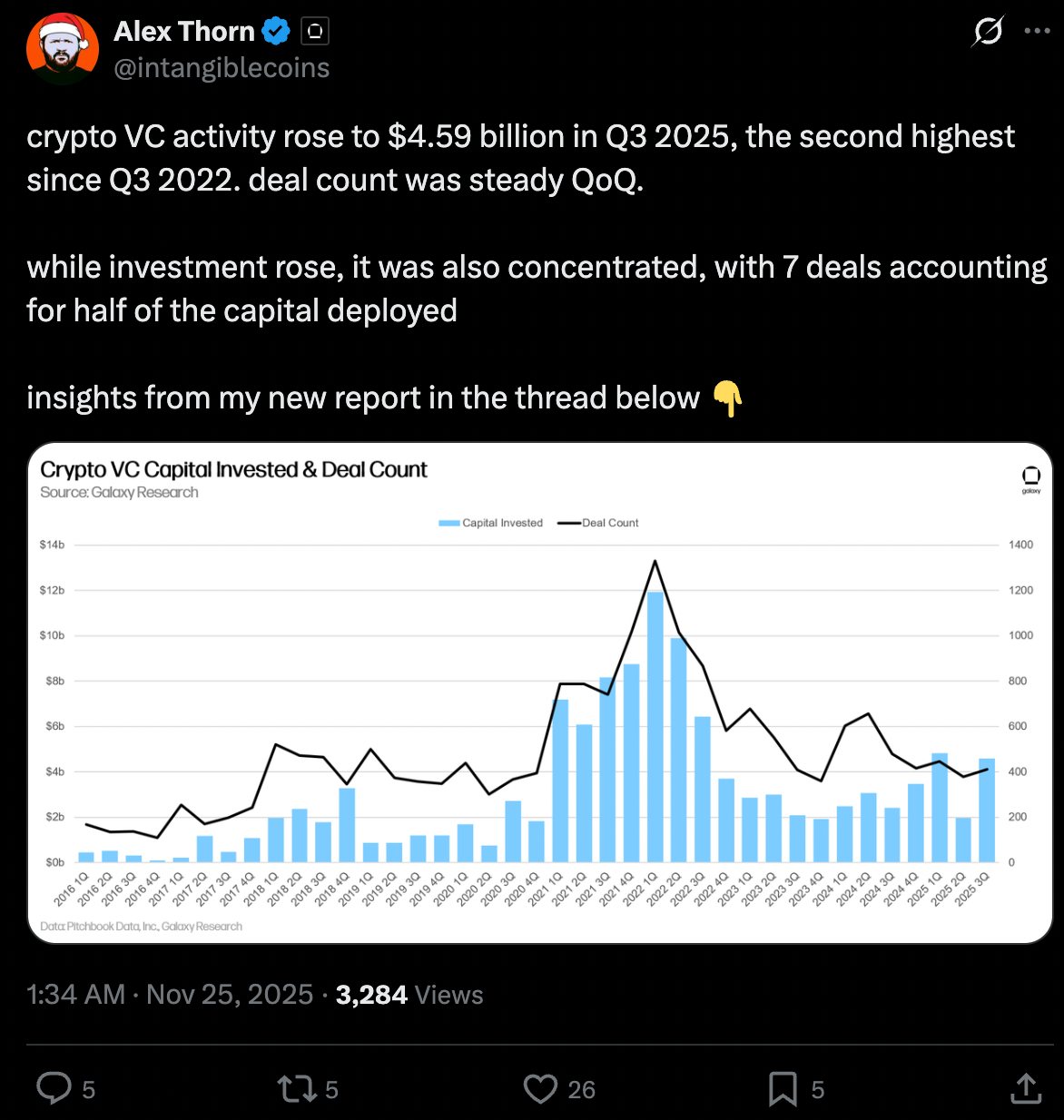

Alex Thorne, head of research at Galaxy, said half of the $4.59 billion raised in the third quarter was concentrated in just seven deals.

“The market downturn creates an increased focus on execution and product resiliency as key metrics that are important, rather than looking at price trends as signals,” said Hashgraph Group’s Diess. “The economic downturn causes investors to focus more on fundamentals than short-term momentum.”

That short-term momentum is often more hype than anything else. And many of the large venture-backed projects that implement TGE have not performed very well this year. This includes PUMP (down over 50% in 2025) and Berachain (down 91% since February launch).

“High volatility and uncertain early-stage valuations are driving significant changes in capital deployment, favoring strategies with shorter liquidity cycles and better price control,” Goldadze added.

Sponsored Sponsored

Lockups and liquidity

One of the most distinctive aspects of the cryptocurrency industry is Token Generation Events (TGEs).

Coinbase, a successor to previous ICOs, is currently promoting TGE after acquiring investor platform Echo for $375 million.

Monad was the first project to launch there, raising $296 million, but more are sure to come.

However, once a token is launched, there are some metrics specific to cryptocurrencies that venture investors should closely monitor.

One is the lockup, in TGE not all tokens are in circulation on the market yet. There is a period of time during which these assets are held. This is designed to better motivate network participants, from team members to community airdrops and foundation initiatives.

Then there is the fully diluted value, or FDV. This is the product of the total number of tokens and the price. This is essentially the market cap of all tokens, even if they are not yet unlocked.

And when the market fluctuates, it can be very difficult and challenging for VCs to predict the potential exit of their tokens.

Recently, Arthur Hayes of Maelstrom Capital went on a rant about lockups specifically related to Monads. As a trader, Hayes clearly doesn’t like this kind of token liquidity.

Sponsored Sponsored

“Given that the average token or stock vesting/lockup period is 12 to 48 months, VCs need to model the expected market conditions when these lockups end,” said Techstars mentor Gordadze. “Entry prices must be set strategically to ensure a profitable exit, and long-term market forecasting is key to closing deals.

The future of crypto VC investment after 2026

When it comes to the subject of market forecasting, VCs certainly love talking about the future. And when it comes to cryptocurrencies, next year looks like it could be even better, given favorable US regulatory measures in 2025. Is it just an investor hopium?

perhaps. However, rose-colored (or green) glasses are always the default mode for VC. Of course, optimism always wins.

“2026 is shaping up to be the year in which real utility is defined. DeFi will make a strong comeback with increased momentum and maturity, and the stablecoin moment will be the backdrop,” Diess said. Stablecoins certainly had their moment this year. That said, stablecoins are the boring infrastructure that will power, for example, the upcoming Polymarket, which uses USDC on Polygon as its main coin and chain.

“Now that stablecoins are finally mainstream and banks are rushing to jump in, the next level will be services for users that leverage these assets behind the scenes,” Goldadze said.

The most important growth areas are likely to lie at the intersection of AI/blockchain and RWA/blockchain, as these represent the greatest opportunities for real-world impact and revenue generation for institutions. ”