T. Rowe Price manages about $1.89 trillion, about 66% of which is tied to relationships with retirement accounts, advisors and institutions that the crypto industry has spent years working towards.

The company’s first crypto product, a spot ETP called TKNZ, began trading on the NYSE Arca on July 16th, jumping straight into the diversified multi-token basket. The basket is the corner of the crypto ETF market that has so far attracted the least amount of money.

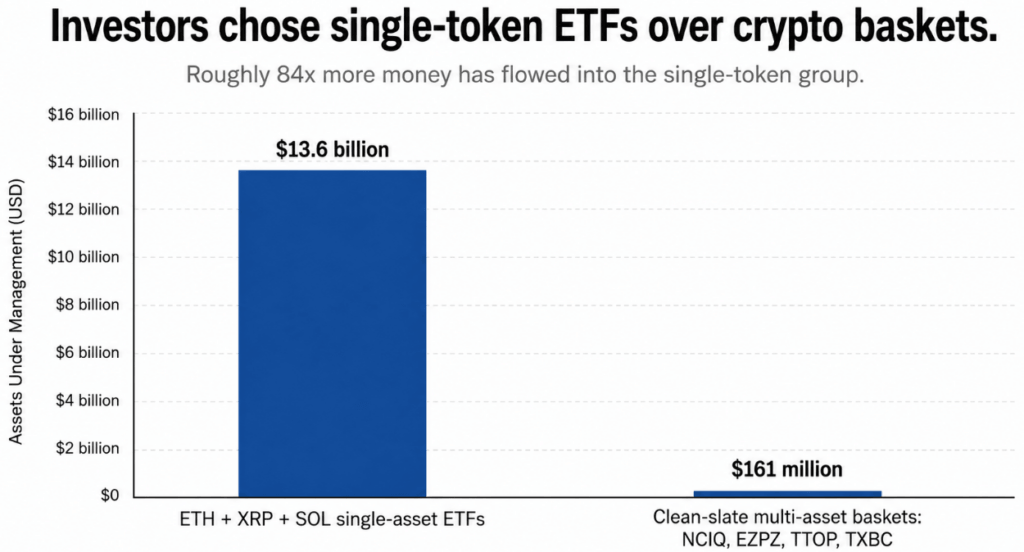

Single-asset spot ETFs tracking Ethereum, XRP, and Solana have raised about $13.6 billion, excluding Bitcoin entirely. Four comparable multi-asset products built from the ground up, NCIQ, EZPZ, TTOP, and TXBC, raised approximately $161 million during the same challenging period.

Gaps of this size will still persist despite timing warnings.

unreasonable forecast

Several prominent cryptocurrency commentators predicted that multi-asset crypto ETFs would be the next catalyst for institutional adoption.

Matt Hogan argued that many traditional investors do not have strong opinions on Ethereum vs. Solana and prefer broad exposure. Roksanna Islam predicted that the sheer number of new crypto ETFs will overwhelm advisors’ due diligence and drive buyers to simpler basket products.

Nate Geraci is bullish on one-click crypto exposure, and James Seifert predicts index-based crypto ETPs will be the dominant category this year.

A common assumption was that professional allocators would eventually stop picking individual tokens and start buying entire asset classes.

As of mid-2025, pensions and endowments will account for less than 5% of Spot Bitcoin ETF assets, with retail investors still dominating the category.

Convicted buyers, especially those hoping for an Ethereum recovery or an XRP payment theory, have little reason to dilute their bets with eight other tokens chosen by someone else.

Cryptocurrencies also lack anything akin to the S&P 500, a widely accepted definition of belonging to an investable market. Every basket has to make controversial decisions about which tokens are considered sufficiently decentralized, liquid enough, or legally eligible.

Purchasing an index transfers the selection of tokens to the person who built the index, and someone else makes the same selection on the purchaser’s behalf.

HashDex’s NCIQ is one of the cheapest baskets with a 0.25% fee, but it still ranks close to 90% of Bitcoin and Ethereum, an exposure that most investors can replicate with two single-asset ETFs and full control over weighting.

Diversifying away from Bitcoin while altcoins lag is a drag, as opposed to a bond allocation that cushions a stock portfolio. Advisors explaining their clients’ stakes to a basket of underperforming tokens are having a difficult conversation.

The Problem What investors expected What happened instead Why buyer mismatch matters Advisors and institutions prefer broad crypto exposure Retail and conviction buyers still dominate Token-specific thesis trumps abstract asset class exposure Weak diversification Baskets reduce single-token risk Many baskets remain heavily weighted BTC/ETH Investors can recreate most exposures with single-asset ETFs There is no crypto “S&P 500” Index exposure feels neutral Token inclusivity remains subjective and debatable Basket purchases outsource token selection Bad timing Altcoins will make the basket look broader and more attractive Altcoins lag while Bitcoin dominates Diversification appeared to be a drag on performance Structural baggage Converted products will validate the category Legacy holders withdrew after ETF conversion Outflow obscured new demand signals

Something new from T. Rowe

Bitwise’s BITW recorded approximately $328 million in post-annual redemptions, while Grayscale’s GDLC experienced large withdrawals after converting to ETF format.

Outflows include a mix of old holders cashing out and new demand decisions, as conversions allow traditional shareholders stuck in old, illiquid structures to finally exit at net asset value.

The weight of this shift still leaves the category looking like a place for investors to retreat.

TKNZ is the first in its category to combine four advantages. T. Rowe brings the relationship between advisor and retirement platform that the original basket theory always envisioned.

It’s also actively managed, allowing you to move weights freely based on fundamentals and momentum, and keep your cash or stablecoins if circumstances change. This is an active alternative to the mechanical holding all eligible tokens approach that older baskets used.

T. Rowe has also been outspoken about the fund’s design, openly touting his judgment on which tokens are worth the money.

This combination leaves TKNZ trying out three different explanations for why the basket is struggling. It is the distributive disparity between investors and issuers, the rejection of a passive basket centered around Bitcoin in particular, or the sheer preference for picking tokens directly.

If TKNZ is still unable to raise any real funds, the third explanation will be much harder to refute.

What T. Law still has to prove

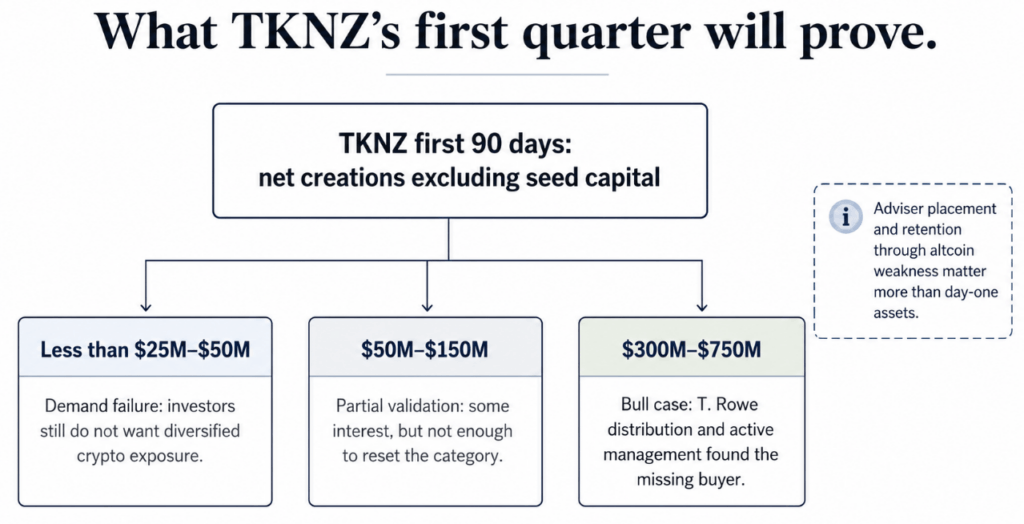

If TKNZ were to raise $300 million to $750 million in net creation, excluding assets launched, in the first quarter, it would demonstrate that T. Rowe’s distribution and active management can reach capital that has been completely missed by crypto-native basket issuers.

Real advisor placement and retention due to altcoin weakness would turn this from one fund’s initial traction to evidence that the basket theory needed the right issuer.

If net creation in T. Rowe’s name remains below approximately $25 million to $50 million, and is fully deployed, the result would be to point out that institutional investor and advisor demand for diverse crypto exposure may still be small, even at meaningful scale.

The proof lies in what TKNZ has raised in the first quarter since seed capital was removed from the count, whether that money moves through the advisor platform, the channel the original thesis always relied on, and whether it continues to stick around during the next rough patch in the altcoin market.

That is the window that will ultimately tell the industry whether professional money wants cryptocurrencies as part of their portfolios.