A recent survey of over 5,700 Bitcoin (BTC) holders revealed a clear disconnect between beliefs and actions in the cryptocurrency space. Nearly 80% of respondents support widespread adoption of cryptocurrencies, while 55% say they rarely or never use digital assets for everyday payments.

This widening gap between beliefs and actual usage suggests that the industry’s biggest challenge is no longer perception or ideological support, but something else.

Most Cryptocurrency Users Support Adoption, But Little Spends: Here’s Why

GoMining’s survey received responses from users in multiple regions. The largest shares were in Europe (45.7%) and North America (40.1%).

Sponsored Sponsored

Participants had a wide range of experience levels, with an almost even split between crypto beginners and those who had been in the market for several years.

This distribution shows that restrictions on cryptocurrency spending are not limited to a single region or user profile. The survey found that cryptocurrency payments remain a niche activity among users.

Only 12% of respondents use cryptocurrencies for daily payments. This number increased slightly to 14.5% on a weekly basis and 18.3% on a monthly basis. Still, the majority report rarely or never using cryptocurrencies.

Spending behavior shows where cryptocurrencies work best as a payment option. Digital goods accounted for the largest share at 47%, followed by game purchases at 37.7% and e-commerce transactions at 35.7%.

This shows that users are already actively using cryptocurrencies in a digital-first environment that natively supports payments. Beyond these spaces, payment utilization decreases significantly.

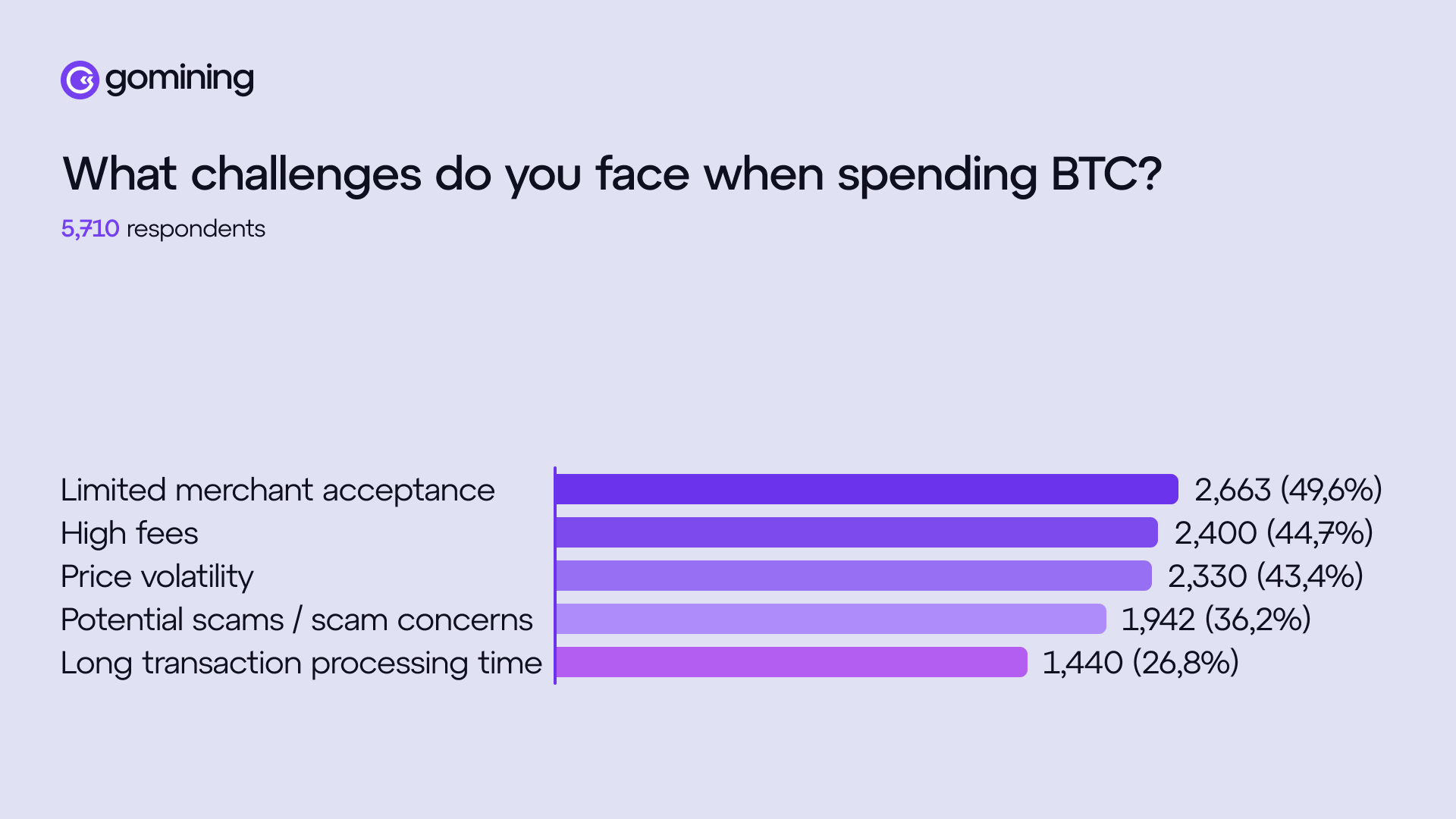

The survey results reveal that infrastructure-related issues remain the main barrier to spending. Respondents cited limited merchant acceptance (49.6%), high fees (44.7%), and volatility (43.4%) as the main reasons for not using cryptocurrencies for payments. Notably, 36.2% of users cited potential fraud as their main reason.

Sponsored Sponsored

Mark Zalan, CEO of GoMining, told BeInCrypto that most users will continue to perceive cryptocurrencies as a novelty if their use involves additional complexities such as choosing a network, managing fees, accounting for price fluctuations, and figuring out how to undo mistakes.

“For everyday users, ‘true usefulness’ begins when cryptocurrencies fade into the background. Once cryptocurrencies are accepted in the places they already shop, costs are clearly competitive, payments are quick, and consumer expectations such as receipts and dispute resolution are supported. To capture that user, crypto payments need to feel as boring and reliable as tapping a card,” he said.

The executive added that the gap appears to be more of a “day-to-day product issue” than a “recruitment issue.”

“People can default to their cards and banking apps and still be open to cryptocurrencies in principle because those options are ubiquitous and feel comfortable, and our findings are consistent with that. When there is interest but patchy acceptance, everyday usage stagnates, costs feel unpredictable, and volatility creates hesitancy,” he said.

Zaran pointed out that the abundance of tokens does not automatically create everyday utility, as most tokens do not remove everyday hassles for ordinary consumers.

Practical utility emerges when cryptocurrencies offer clear structural advantages such as cross-border value transfer, faster settlement, and programmability. As a result, the industry has increasingly focused on payment rails and integration, rather than expecting users to actively manage and navigate dozens of different assets.

Sponsored Sponsored

Bitcoin payments face incentive-driven expectations from users

Meanwhile, the study investigated the actual factors that lead users to choose cryptocurrencies over traditional payment methods. Privacy and security emerged as a key factor, cited by 46.4% of respondents. Perks and discounts are a close second at 45.4%.

Users were clear about what they wanted when it came to Bitcoin payments. 62.6% pointed to lower fees. Incentives such as rewards and cashback followed at 55.2%, followed by broad acceptance by merchants at 51.4%.

Notably, nearly half of respondents said they expected to receive a yield or reward on every dollar they spent. This highlights how incentive-driven expectations are.

The data also shows a major shift in how users think about Bitcoin itself. While many still describe themselves as long-term holders, the growing interest in mining, revenue-generating products, and tokenized hashrates suggests they prefer Bitcoin actively producing profits rather than sitting in a wallet.

In this context, payments are increasingly being seen as another opportunity to expand asset holdings. Zalan said incentives are a standard mechanism in payments.

He explained that traditional systems also use incentive structures. They provide rewards to consumers, economic benefits to publishers, and predictable payments to merchants.

“It is unrealistic to expect crypto payments to scale without a similar ‘worth switching’ dynamic. What the incentives reveal is where the remaining friction lies: if the experience is already cheaper, faster and more widely accepted, Incentives become less important. For now, incentives cover switching costs and help people build habits, while the ecosystem bridges the gap between acceptance, refund/resource expectations, and ‘works’ checkout flows,” the CEO said.

Sponsored Sponsored

Respondents also outlined that they would consider using Bitcoin in the future. Daily expenses were the most common at 69.4%. This was followed by games and digital entertainment at 47.3% and high-value or luxury goods at 42.9%.

From a user perspective, Bitcoin is no longer limited to niche uses, but is increasingly seen as a viable option for everyday spending. But this also raises serious concerns. If Bitcoin succeeds as an everyday payment method, will it strengthen its role as a store of value, or risk diluting its story?

Zaran believes broader payment utilities will ultimately strengthen Bitcoin’s role as a store of value. He explained that store of value status is ultimately the result of social and market coordination.

It is shaped by liquidity, reliable payments, and the degree to which assets are integrated into the real-world financial system. According to him,

“The more frequently Bitcoin can be used (even through layers like Lightning and cards), the more it behaves like a durable financial asset with resilient demand and surrounding infrastructure.”

He stressed that concerns about “dilution” often confuse spending with loss of faith. In mature financial systems, long-term holding and everyday use are not mutually exclusive, as long as the infrastructure removes friction.

Looking ahead to 2026, Zaran outlined a more realistic outcome. That’s because Bitcoin acts as the reserve and settlement anchor, and a user-friendly payment layer handles checkout, allowing users to transact without having to think about blocks, fees, or timing.