Cryptocurrency market capitalization is down more than 36% year-over-year, the altcoin complex is about 45% below its October 2025 peak, and Bitcoin is off to its worst start to the year in more than a decade, with funds going to AI stocks and large IPOs.

After three years of waiting for a widespread altseason to arrive, altcoin traders have experienced a rapidly declining narrative, an unlock-driven selloff, a rotation of meme coins that rewarded a few early buyers, and a rally that fizzled out before most participants could participate.

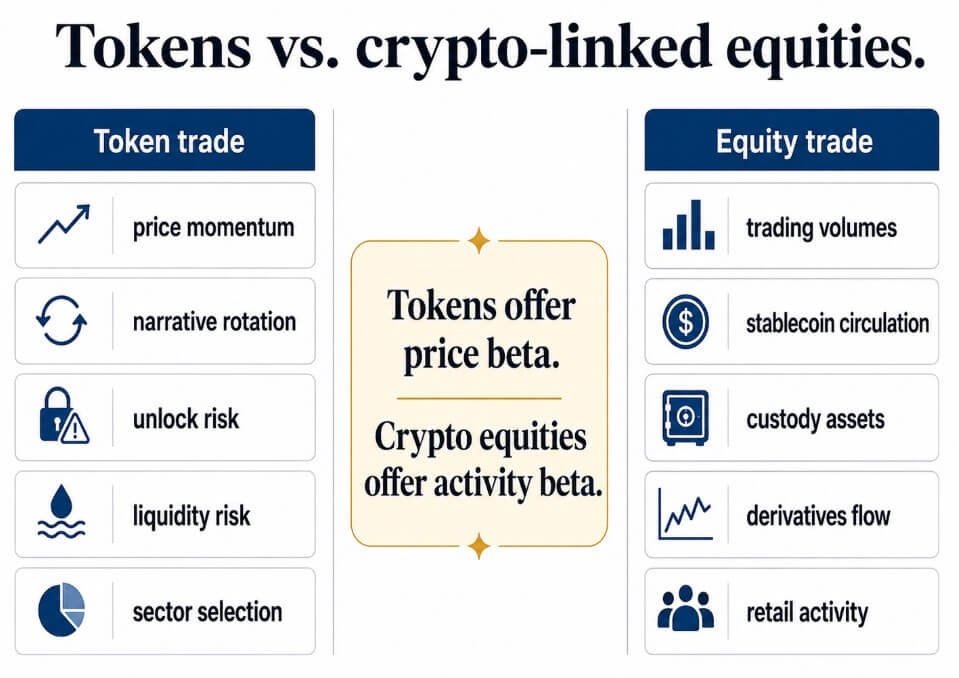

Some investors are now questioning whether owning a company that profits from crypto activity is a cleaner deal than picking the next token.

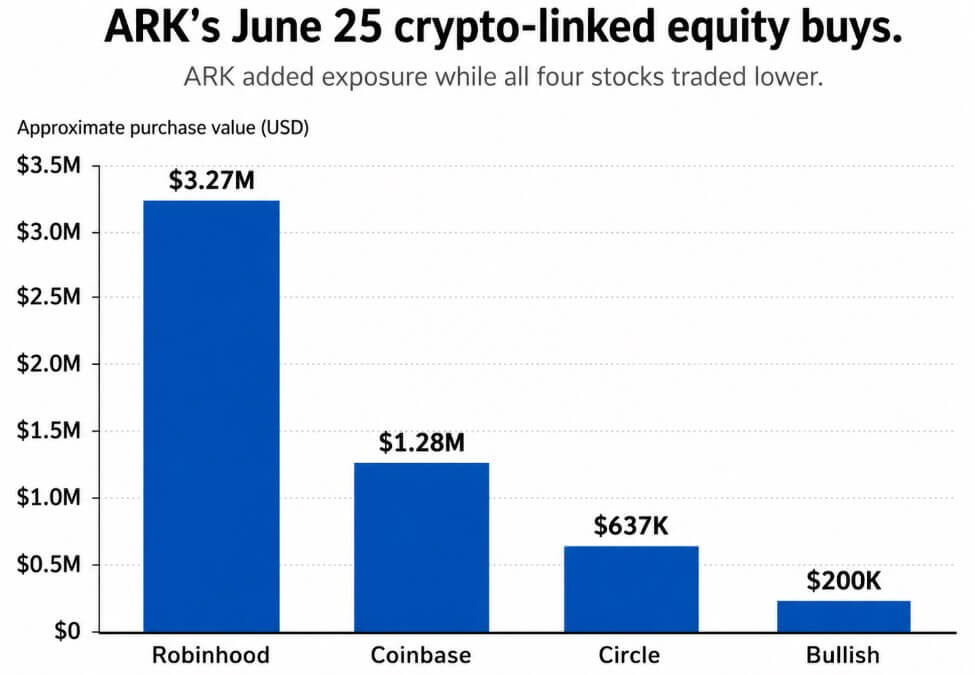

On June 25th, ARK’s ETF bought approximately $5.4 million in four crypto-related stocks, even though all four stocks were down.

The total purchase price was approximately $1.28 million on Coinbase, $637,455 on Circle, $199,895 on Bullish, and $3.27 million on Robinhood. Cathie Wood was buying on weakness, and the stocks she picked were companies that made money from crypto activity.

Cryptocurrency-linked stocks provide investors with exposure to cryptocurrency activities such as trading volume, stablecoin circulation, assets under custody, derivatives flows, and retail speculation.

The two bets have diverged sharply in the low-energy battles that have defined the past three years.

What each name represents

Coinbase’s Q1 update reports that the market share of cryptocurrency trading volume is 8.6%, derivatives trading volume is up 169% year over year on a trailing 12-month basis, and 12% of the world’s crypto assets under custody and over 25% of USDC in circulation are held in Coinbase products.

These structural positioning numbers reflect what Coinbase collects when trading volume returns and how exposed it is when trading volume pulls back.

Coinbase’s trading revenue for the period fell about 40% to $756 million, with total revenue down to $1.43 billion from $2.03 billion in the year-ago period, and the company posted its second consecutive quarterly loss as trading momentum waned.

In the first quarter, Circle’s USDC in circulation reached $77 billion, an increase of 28% year-on-year, and on-chain USDC trading volume increased by 263% to $21.5 trillion.

Total revenue and reserve fund income increased 20% to $694 million due to higher USDC average circulation, partially offset by lower reserve fund returns. According to live data as of June 25, there is $73.6 billion in USDC in circulation.

The economics of the Circle operate on circulation scale, reserve yield, and distribution arrangements, and the altcoin narrative cycle is not important in its model.

Every 100 basis points change in yield on $77 billion of total reserves in circulation equates to approximately $770 million annualized before expenses.

CRCL trades as a bet on interest rates and dollar liquidity overlaid on a stablecoin adoption bet, with a risk profile shaped primarily by interest rates and regulatory outcomes.

Robinhood’s crypto revenue in the first quarter was down 47% year over year to $134 million, with crypto notional trading volume on the Robinhood app down 48%, with an additional $42 billion from Bitstamp bringing total notional value to $66 billion.

The bulls rounded out the basket on the institutional side, which reported first-quarter digital asset sales of $51.8 billion, adjusted EBITDA of $35.1 million, and BTC options open interest market share of 14% in April.

Company Cryptocurrency Exposure Must ReturnMajor RisksCoinbase Exchange Fees, Custody, Derivatives, Economics of USDCTrading Volumes, Institutional Investor Activities, Retail SpeculationRevenues Decline Rapidly as Trading Volumes DecreaseCircleUSDC Distribution, Reserve Income, Payment InfrastructureStable Coin Adoption, Support Rates, Regulatory Clarity Robinhood Retail Crypto Brokerage, App-Based Speculation, Bitstamp Trading Volumes Retail Risk Appetite and Cryptocurrency Notional Capital Trading Volumes Retail Flows May Disappear Quickly in Low-Energy Markets Bullish Institutional Exchange Infrastructure, Digital Asset Sales, BTC Options Institutional Trading Demand and Derivatives Activity Institutional Trading Volumes Shrink as Cryptocurrency Sentiment Weakens

The subsequent transactions

In the bullish case, retail speculation returns, derivatives activity picks up, and stablecoin supply continues to expand.

Under these circumstances, exchanges and brokers may reprice before widespread altcoin rotation becomes apparent, as trading revenue and profit estimates may reset faster than the token’s narrative has formed.

Adding 10% to Coinbase’s first quarter trading revenue base of $756 million would mean an increase of approximately $76 million each quarter, and that number would reach $189 million at 25%.

Companies that collect fees from new activity can move forward with estimates before anyone agrees on which L1, L2, or sector tokens to own.

In the bearish case, AI, IPOs, and public market stocks continue to absorb capital, crypto trading volumes remain thin, and the narrative volatility that has characterized the past three years continues.

As recent results from Coinbase and Robinhood have already shown, when activity wanes, publicly traded crypto companies feel it directly in their earnings.

The circle relies on USDC’s outstanding holdings and reserve yields remaining supportive, and the bullishness relies on institutional trading demand, which could itself contract if broader crypto sentiment changes.

If the crypto winter drags on, these companies’ revenues will be well below full capacity.

Older versions of rebound theory trading required accepting liquidity risks, unlocking schedules, story declines, the possibility that the rotation would pass through a completely different sector, and selecting tokens before retailers could find them. The stock version trades the rise in token levels for a more readable bet on the activity itself.

Whether this cycle’s rotation looks like a broad alternative season in 2021, or something narrower, faster and harder to ride from the token side, is a question with Wood already positioned on the stock side.