Hyperliquid Strategies has built its finances around HYPE, but its first SEC filings show the strategy is already facing fundamental challenges.

The company hopes to accumulate more tokens for shareholders, but warns investors that it may need to sell HYPE for future financing, paralleling its long-term accumulation goals with the practical limits of market liquidity.

Hyperliquid Strategies says its primary objective of accumulating HYPE tokens on behalf of shareholders will be funded by proceeds from the closing PIPE and future funding.

The company has established a commitment equity facility with Chardan that can direct the sale of up to $1 billion of common stock, with the company managing the timing of the sale.

The PIPE package that seeded this strategy includes approximately $299.9 million in cash and 12,517,592 HYPE tokens valued at $580.5 million at the time of signing, for a total fair value before costs of $880.4 million.

By the time the transaction closed, these same HYPE tokens were worth $411.3 million, resulting in a loss of $169.2 million from the company’s prior contribution before purchasing one additional token.

As of May 14, HyperLiquid Strategies held approximately 20.8 million HYPE, which is the largest HYPE position among U.S. publicly traded companies.

The filing includes a warning that the company may sell HYPE at a disadvantageous price during periods of market instability.

Item Diagram Why It Matters Strategic Goals Accumulating HYPE for Shareholders Turning HYPE into a Public Company Financial Asset Equity Facility Giving the Company a Repeatable Capital Raising Path Through Up to $1 Billion in Common Stock Sale PIPE Cash $299.9 Million Immediate Purchase Ability $12.52 Million Contributed by HYPE at Signing HYPE Value Will Be $580.5 Million Directly Funding Financial Strategy Token Exposure HYPE Value At Closing Price $411.3M Showing Market Value Risk Before New Accumulation Contribution Loss $169.2MD Demonstrating How Quickly The Token Volatility Will Reach The Wrapper HYPE Holding As Of May $1,420.8 million HYPE baseline for future accumulation or dilution analysis

Second wrapper pending approval

Grayscale filed a preliminary prospectus on May 26 for a proposed HyperLiquid Staking ETF, formerly known as the “Grayscale HYPE ETF.”

The document itself states that the trust cannot sell its securities until the registration statement becomes effective, meaning the product currently exists only on paper.

The trust directly owns HYPE and aims to reflect the per-share value of HYPE, including staking fees if the fund engages in staking. According to the filing, staking takes approximately 24 hours and unstaking takes approximately 7 days, depending on demand.

This slot will sit between the trust and its stake, HYPE’s liquidity, during times of market stress when equity creation, redemption and hedging mechanisms are paramount.

Hyperliquid had 33 validators as of June 9, and Grayscale’s filing warns that such a small set of validators could work together to influence trading orders, market parameters, listing and delisting decisions, and governance itself.

The filing supports that warning with two incidents already on the record. In March 2025, an attacker inflated the price of the JellyJelly token by 429%, costing HLP $12 million, and validators delisted the token and closed their positions in about two minutes.

In November 2025, a POPCAT manipulation incident resulted in an estimated loss of $4.9 million, and HyperLiquid suspended withdrawals while the company responded.

The filing cites both incidents as examples of how validators and protocol operators can quickly work together under market stress, and warns that the same speed could deepen centralization concerns.

Supply overhang behind buying

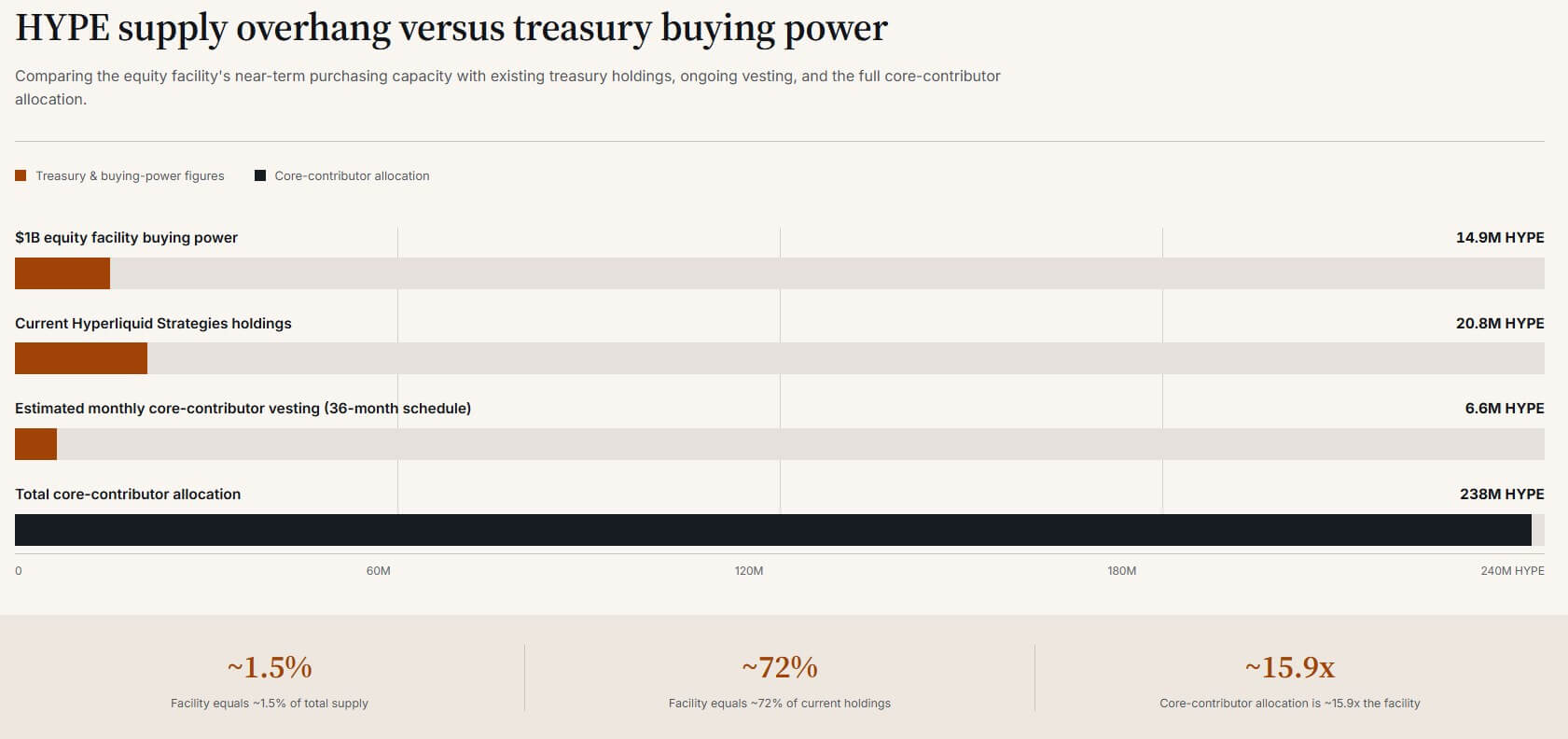

The protocol caps the total supply of HYPE at 1 billion tokens, of which 310 million tokens have already been distributed and unlocked through Genesis, 238 million tokens are held by core contributors and vest monthly from November 2025 through 2027 and 2028, and a further 388 million tokens are set aside for future emissions and community rewards.

This 238 million core contributor allocation is worth approximately $15.9 billion at a HYPE price of around $67, and is approximately 15.9 times the $1 billion available for HyperLiquid Strategies to acquire HYPE.

Once the facility is fully utilized, the company will add approximately 14.9 million tokens to its holdings, representing just under 1.5% of the total supply and approximately 72% of its current position.

Spreading the core contributor unlocks over 36 months results in monthly vesting of nearly 6.6 million HYPE, equivalent to approximately $443 million at current prices. This is a monthly figure that represents approximately 44% of the total purchasing power of the $1 billion facility.

At the time of writing, DefiLlama is tracking HyperLiquid with approximately $10.4 billion in open interest against HYPE’s $14.9 billion market cap, making the open interest approximately 70% of the token’s market cap.

The 30-day perpetual trading volume reached $210.1 billion, more than 20 times the open interest, and the 30-day liquidating trading volume totaled $2.6 billion, about 25% of the open interest itself.

These numbers represent an environment where HYPE’s sales potential is tested in a venue operating on a fixed margin and fixed clearing basis, with both Treasury filings and ETF prospectuses.

What will be decided in the next few months?

The bullish path is that HyperLiquid Strategies raises equity at favorable levels relative to net asset value, that staking yields make HYPE exposure more sticky for holders, and that HYPE’s market capitalization expands rapidly as liquidation volumes decline as a share of open interest.

Once Grayscale’s proposed fund launches, its premiums and discounts will remain steep and HYPE will begin trading like a trusted public market financial asset with a value story that extends beyond its PERP venue.

On the bearish path, the price of HYPE declines as open interest and liquidations increase, causing HyperLiquid Strategies shares to fall below their net asset value, leading to further dilution from issuance.

Spot liquidity will become thin enough to strain authorized participants’ hedges, spreads will widen around the proposed fund, and HYPE’s spot trading volume will fall below the size needed to absorb monthly vesting without moving prices.

Access to public markets amplifies token volatility, and these wrappers promise to reduce risk.

Indicators to watchBullish pathBearish pathWhy is it important?Hyper Liquid Strategies shares trade at NAV premium or near NAVTrade below NAVDetermine whether stock issuance is accretive or dilutiveDetermine whether HYPE market capitalization and open interest interest Market capitalization is faster than OIO 30-day liquidation value/OIF is currently ~25% below the level PERP measures intra-venue stress ETF premium/discount (if initiated) Tight Spreads Test whether persistent discounts or wide spread wrappers can track HYPE in volatile conditions AP and Market Maker Hedging Orderly Liquidity Hedging Friction and Spread Widening Key Risks of Grayscale Filing Monthly Vesting Absorb Spot Demand Unlocks Vesting Overwhelms Spot Liquidity Treasury/ETF Tests Whether Demand Can Offset Supply Pressures Validator Intervention No Emergency Adjustments New Delistings, Suspensions, Bridging Incidents Determining Whether “Protective Adjustments” Become Centralization Risks

Hyperliquid’s validator interventions in JellyJelly and POPCAT can just as easily be read as protective as they can be read as centralized, and the record to date supports both readings.

Both the treasury company and the proposed staking ETF offer open market access to the tokens, although the tokens’ documentation acknowledges that they may not be available for sale at the point of peak access.