BlackRock’s digital asset franchise crossed the threshold in the first quarter, proving to Wall Street that it’s a real fee line for the world’s largest asset manager.

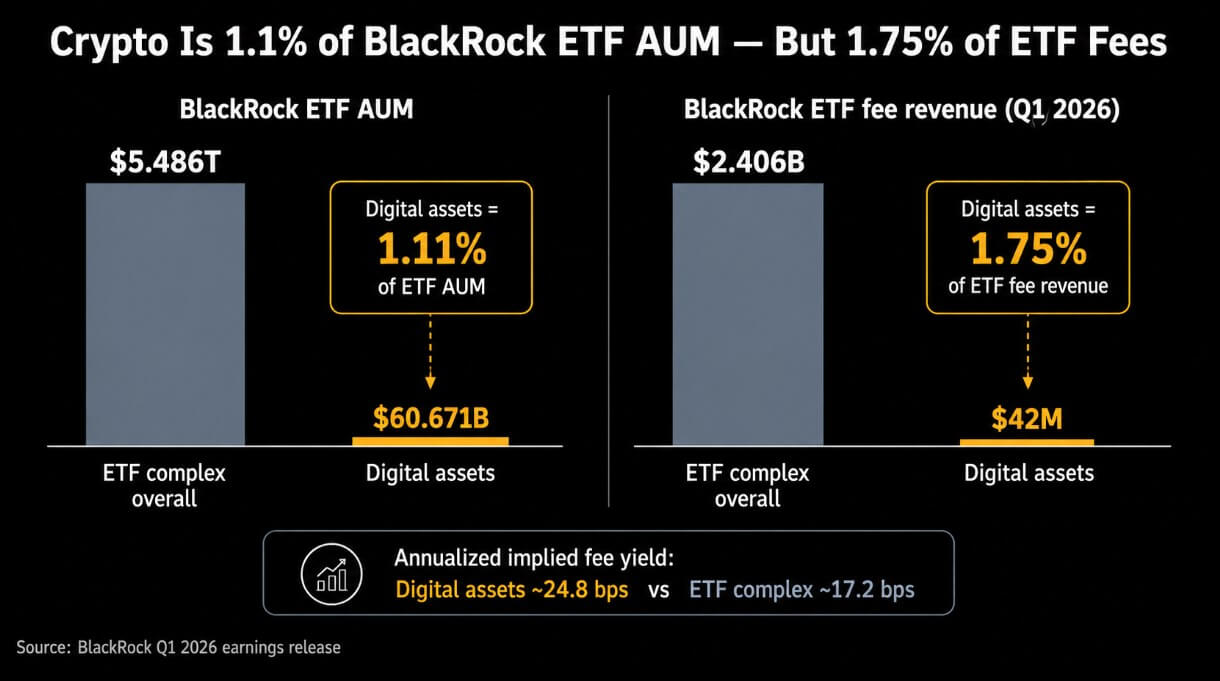

The company’s digital asset products generated $42 million in investment advisory, management fees and securities lending revenue during the quarter. Almost any way you measure its weight in BlackRock economics, that number is relatively small.

The ETF complex housing these products generated more than $2.4 billion during the same period. Digital assets account for nearly $60.7 billion of BlackRock’s $5.48 trillion in ETF assets under management, or 1.11% of the total. On a fee basis, the share rose slightly to 1.75%.

The difference between AUM share and revenue share favors cryptocurrencies.

Using BlackRock’s average AUM numbers for the quarter, the digital asset line ran at an annualized rate of approximately 24.8 basis points, compared to approximately 17.2 basis points for the entire ETF complex.

Cryptocurrencies are high-fee products that exist within a giant low-fee machine, which is why they capture a disproportionate share of the revenue pie despite their modest asset footprint.

The problem is that the “imbalance” only comes from such a small base, as iShares had a record $132 billion in net inflows in the first quarter, with net new base fees doubling year-over-year.

Contrary to that momentum, the $42 million in virtual currency is financially insignificant, and the first quarter revealed how dependent the revenue line is on asset prices.

BlackRock’s digital asset products recorded net inflows of $935 million in the quarter, representing just 0.71% of total ETF inflows. BlackRock recorded nearly $18.7 billion in negative market volatility in the digital asset category, with assets under management falling from $78.4 billion at the end of 2025 to $60.6 billion as of March 31.

This pattern reframes adoption theory, as the fee base for products like IBIT fluctuates in response to the price of Bitcoin, while advisor approvals and platform listings are secondary variables.

BlackRock’s crypto revenue will continue to fluctuate quarterly, driven by beta, until its digital assets under management are large enough to offset price fluctuations with inflows.

From flagship to franchise

As of April 29, IBIT had approximately $61.7 billion in net assets with a 0.25% sponsorship fee, and BlackRock calls it the most traded spot Bitcoin ETP in the U.S. since its launch.

At this asset level, IBIT represents approximately $152.9 million in annual sponsorship revenue. However, BlackRock does not disclose product-level revenue by ticker, and the $42 million figure covers the entire digital assets segment for the entire quarter.

Product Asset Class Net Worth Fee Strategic Role IBITBitcoin~$61.7B0.25%Main scale product. BlackRock’s Crypto ETF Franchise Main Driver ETHA Ethereum>$7.0 Billion 0.25% Core Ethereum Exposure. Second Leg of Franchise ETHB Gains Ethereum in Article $594.5MN/A High Value Wrapper Tied to ETH Exposure and Staking Rewards Total — ~$68.8B — BlackRock’s Three Flagship US Crypto Products. Approximately 13.4% more digital assets under management than March 31st

ETHA, the iShares Ethereum Trust ETF, had over $7 billion in net assets with the same 0.25% fee as of April 29. ETHB, the iShares Stake Ethereum Trust ETF, was launched on February 18th and raised $594.5 million.

ETHB targets Ethereum price performance and staking rewards, falling into a category that goes beyond plain vanilla spot exposure.

By late April, BlackRock’s three main U.S. crypto products combined had net assets of about $68.8 billion, about 13.4% more than the company’s digital assets under management as of March 31.

If the next phase of crypto ETF monetization comes from richer product structures such as income, staking, and multi-asset exposure, then maintaining the 24.8 basis points yield will be a central execution challenge for the franchise.

Price war, distribution fluctuations

Morgan Stanley launched MSBT on April 8th with a sponsorship fee of 0.14%, which it describes as the lowest sponsorship fee for a U.S.-traded Bitcoin ETP at launch and 11 basis points below IBIT.

Charles Schwab announced on April 16 that it will begin rolling out direct Bitcoin and Ethereum trading for retail customers with a fee of 75 basis points per transaction. Schwab clients already own about 20% of the spot crypto ETP market.

Goldman Sachs has filed for a Bitcoin Premium Income ETF, converting it into an options-based income product that differentiates its Bitcoin exposure.

None of these moves will take away IBIT’s scale advantage or BlackRock’s distribution depth in the short term. With total assets under management of $13.895 trillion, BlackRock has IBIT’s liquidity profile that new entrants cannot easily imitate.

These moves create an arc of competition with more issuers, access to more intermediaries, more product differentiation, and narrower margins. This is how fee compression happened in every other ETF category that reached critical mass.

how math is solved

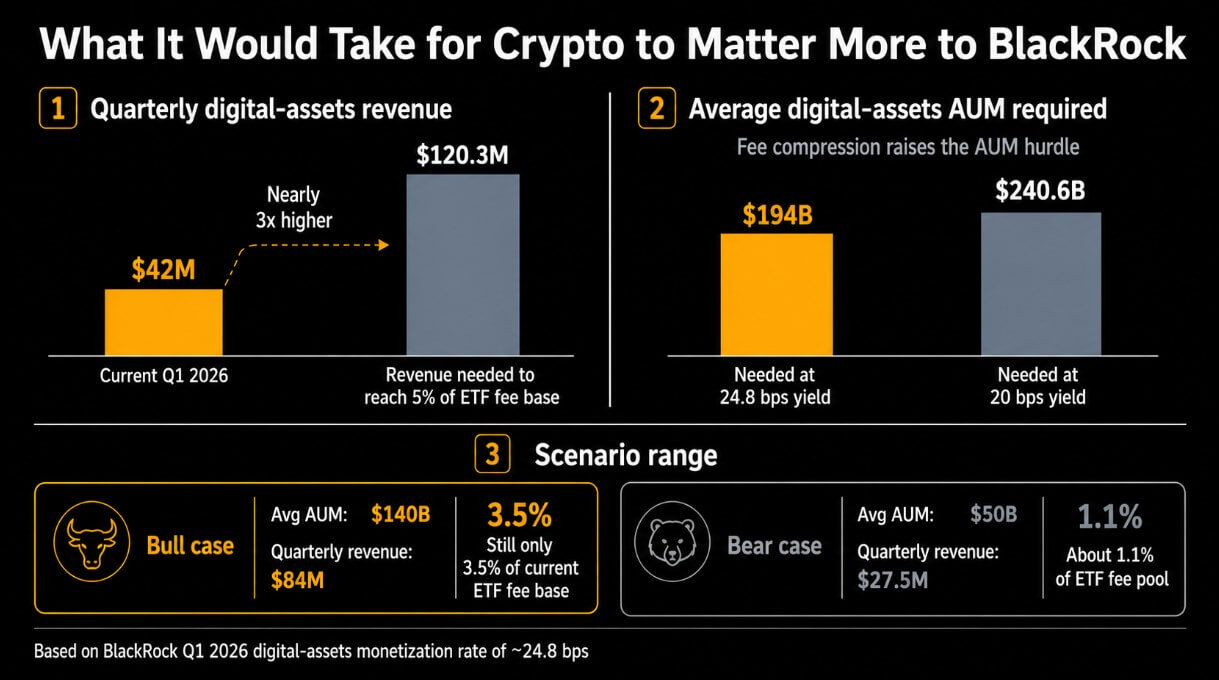

BlackRock’s first quarter realized digital asset monetization rate was approximately 24.8 basis points, with each $10 billion increase in average digital asset AUM increasing annual revenue by approximately $24.8 million.

To reach BlackRock’s current ETF fee base of 5% (approximately $120.3 million per quarter), that yield would require approximately $194 billion in average digital assets under management. If fee compression increases the realized yield by 20 basis points, the required AUM would increase to approximately $240.6 billion.

In any case, for the franchise to contribute 5% to BlackRock’s ETF economy, it would need to be nearly three times its current average.

The bullish path runs through a recovery in asset prices, increased adoption of advisors beyond advanced investors, and richer product structures like ETHB with holding fee yields above the average ETF floor.

Under this scenario, average digital assets under management would reach approximately $140 billion and quarterly revenue would increase toward $84 million, which would still be only 3.5% of BlackRock’s current ETF fee base.

The bearish path follows falling crypto prices, reduced capital inflows and the first round of fee cuts, pushing average assets under management to about $50 billion and quarterly revenue to about $27.5 million, with digital assets returning to about 1.1% of BlackRock’s ETF fee pool. This is almost indistinguishable from the noise in the company’s income statement.

The distance between these two endpoints is large, and asset prices are the key variable for both. No amount of product innovation can make up for $18 billion in quarterly market fluctuations in the short term.

Tougher competition for BlackRock’s crypto-related ETPs remains unresolved and will be determined by price levels and fee schedules.