K Wave Media is yet another example of corporate Bitcoin trading stress.

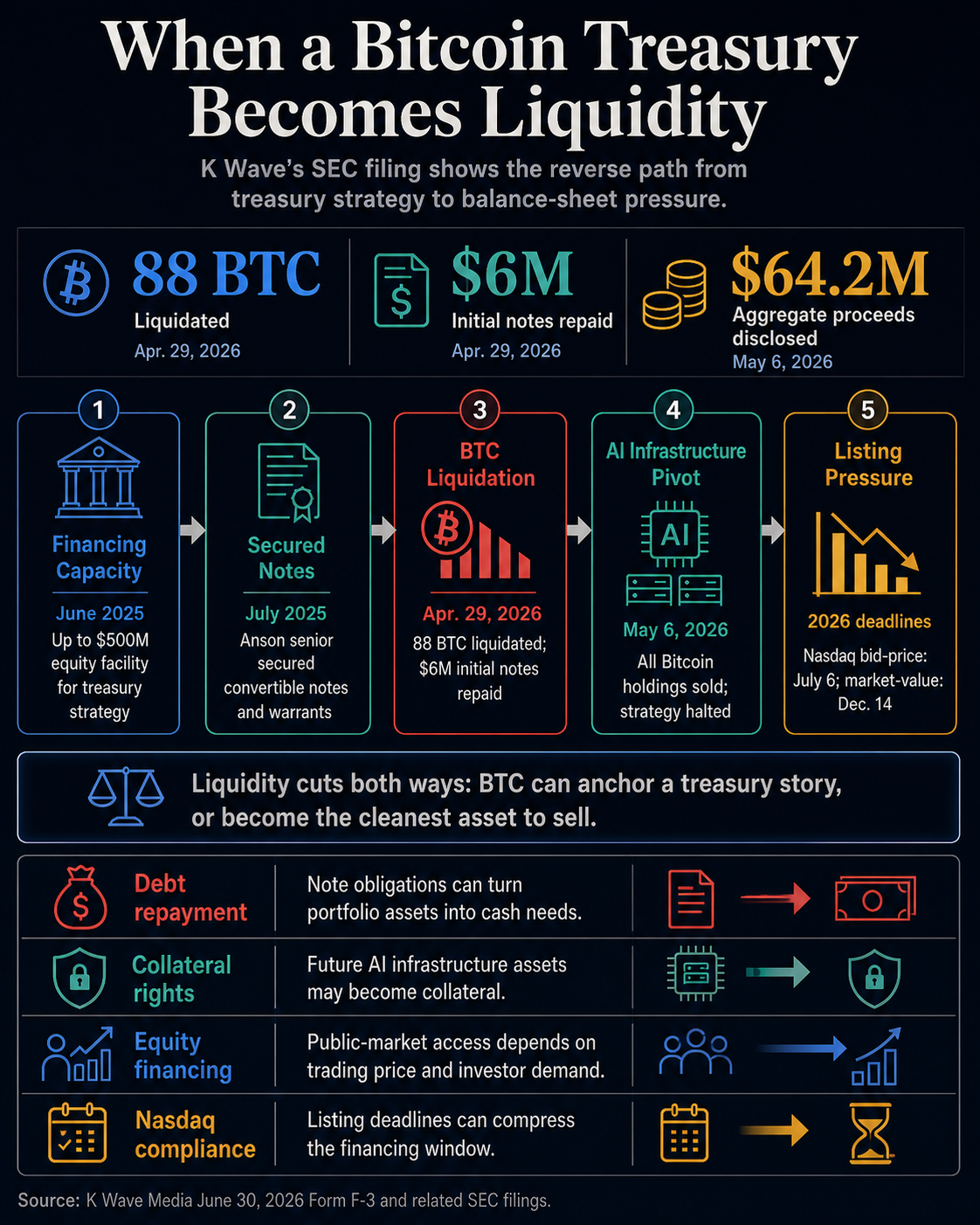

The Nasdaq-listed company disclosed in its Form F-3 dated June 30 that it sold all of its Bitcoin holdings on May 6, and said the sale resulted in total proceeds of $64.2 million.

The filing also states that K Wave liquidated 88 Bitcoin pursuant to an April 29 amendment to its securities purchase agreement with Anson Funds and used a portion of the transaction to repay the $6 million original note.

The filing frames the sale through disclosure of financing, collateral and strategic priorities, rather than an explicit mandatory sale statement. Its value lies in the mechanics it reveals. In other words, as funding priorities change, Bitcoin’s balance sheet could move from a perpetual reserve narrative to a liquid asset.

K Wave said it has not completely abandoned its plans, but said its financial strategy has been suspended while it focuses on AI infrastructure. The differences bring to the fore the company’s financing documents, collateral language and Nasdaq compliance issues.

For investors who have been rewarding public companies that announce Bitcoin purchases, K Wave is the opposite case. The filing points to a weaker version of the Treasury transaction, with the key question being whether the company’s capital structure allows it to continue holding if debt, collateral and listing rules become more stringent.

This filing moves Bitcoin from a financial story to a balance sheet story.

K Wave’s Bitcoin plan started with the ability to raise capital. The June 2025 filing described a standby stock purchase agreement with Bitcoin Strategic Reserve KWM LLC that conditionally gave the company the right to sell up to $500 million in common stock.

Subsequent registration documents state that the proceeds of the sale to Bitcoin Strategic are expected to be used primarily for working capital, general corporate purposes, and the implementation of the company’s financial strategy.

F-3 on June 30th shows how far that structure has advanced by 2026. K-Wave announced that it entered into a securities purchase agreement with Anson Funds in July 2025, under which the company agreed to issue senior secured convertible bonds and stock acquisition rights.

The initial closing generated gross proceeds of $15 million through notes and warrants. This structure also allows for the possibility of issuing additional notes and warrants with conditions.

The April 29th amendment marks a turning point. According to F-3, K Wave liquidated 88 Bitcoins held in the Treasury and repaid the original $6 million note.

The same amendment permitted proceeds from future sales of additional securities under the Anson Agreement to be used for AI infrastructure assets. These AI infrastructure assets serve as collateral under the company’s security agreements.

The essence of market structure is straightforward. The Bitcoin Treasury was sitting on the balance sheet of a publicly traded company that also included convertible bonds, warrants, futures sales, security interests, and new business plans built around AI infrastructure.

The company also said in the filing that it sold all of its Bitcoin holdings on May 6. The filing shows a $64.2 million revenue figure separate from the 88BTC liquidation disclosure, so this figure is best read as the company’s stated total revenue rather than its own price calculation.

The direction of travel is a key point in Treasury trading. K Wave has announced that it will exit Bitcoin completely while shifting its fundraising capabilities to other capital-intensive strategies.

Debt and collateral change the meaning of Bitcoin reserves

Bitcoin treasury companies often present BTC as strategic reserves. K Wave’s filings demonstrate how quickly the language can become complex when reserves are attached to debt documents.

The Anson notes contained conversion rights for the common stock and an alternative conversion mechanism tied to the transaction price. The filing also states that the bonds will not bear interest unless a default occurs, in which case interest will accrue at 12% per year retroactively from the time of issuance.

The document also describes default provisions that may result in acceleration of unpaid principal, unpaid interest and other amounts.

Collateral language is particularly important. F-3 stated that if K-Wave were to default on its collateral obligations, the secured parties would have exclusive control of the collateral and the right to sell, dispose of or transfer it until the collateral obligations are paid in full.

If these remedies are inadequate, K Wave will remain liable for the failure.

The filing provides no evidence that the Bitcoin sale was due to a default, and illustrates why the term “reserves” can be misleading for small financial companies funding strategies through convertible notes, stock options, equity facilities, and secured debt.

Reserves are strategic in some respects and economical in others.

K Wave’s move to AI infrastructure has made that point even clearer. In a May 4 presentation, the company said it was directing its remaining funding capacity toward AI infrastructure and was tying this transition to debt reduction.

The F-3 then secured future AI infrastructure assets under security agreements.

It causes a big conflict. Bitcoin competed with debt repayments, collateral packages, and attempts by companies to reposition themselves around data centers, GPU infrastructure, and AI computing.

These disclosures turn the sale of Bitcoin into part of a broader capital allocation sequence, allowing notes to be paid off, collateral to be restructured, financing options maintained, and a new infrastructure theory to be moved.

Funding window becomes important due to Nasdaq pressure

K Wave’s public market position added additional pressure.

F-3 said Nasdaq notified the company in January that it no longer met the exchange’s $1 minimum bid requirement because the closing bid price was below the threshold from Nov. 20, 2025 to Jan. 6, 2026.

K Wave had until July 6, 2026 to regain compliance. The company said it is considering options such as a reverse stock split, subject to shareholder approval.

A second shortage followed in June. Nasdaq told K-Wave that the company’s common stock does not meet the $15 million minimum market capitalization requirement for publicly traded shares for the period May 4 to June 15.

According to the F-3 and June 18 filing, the company had until Dec. 14, 2026 to regain compliance.

The June 30 registration statement states that K Wave’s common stock closed at $0.164 on June 29. Its stock price is more than the color of the market. For companies whose financial strategies rely on public market financing tools, the actual funding available is determined by transaction price, listing status, and investor appetite.

This is what separates small finance firms from the industry’s largest companies. Large holders with abundant liquidity and repeated access to capital markets may be able to continue adding Bitcoin during volatile times.

Smaller issuers may face a different equation. Falling stock prices can weaken equity issuance, make conversion conditions more important, center collateral, and force corporate action while management tries to protect its strategic narrative.

K Wave’s filing indicates that the transaction can be reversed through the normal public company route. Debts are fixed. The accompanying package will be changed. New uses for the proceeds will emerge. The listing deadline is approaching. Financial reserves become part of a broader capital allocation problem.

That progress is a live signal for the rest of the cohort. As funding documents, listing notices, and collateral packages begin to move together, investors will need to decide whether Bitcoin will remain a protected financial asset or become the most liquid asset on the balance sheet.

Broader Bitcoin Treasuries Trading is Moving from Accumulation to Persistence

K-Wave’s exit comes as investors are already rethinking how they evaluate companies’ Bitcoin strategies.

CryptoSlate has been tracking the shift in headlines from BTC accumulation to issues such as financing, dilution, debt, and whether companies can withstand stress. CryptoSlate noted in May that Bitcoin government bond trading is facing a stress test as some corporate holders use BTC to raise cash, repay debt, and manage funds.

Just recently, CryptoSlate reported that investors are focusing on government bond companies that rely on dilution to continue buying.

Bitcoin remains the reference asset for the entire transaction. According to CryptoSlate’s July 2 Bitcoin market data, BTC is worth nearly $60,000, has a market capitalization of about $1.21 trillion, and commands about 58% of the overall crypto market. Therefore, the assets remain large and liquid enough to anchor the corporate financial story. This liquidity is also why it can become an asset that is sold if another obligation takes precedence.

The next test will be more than just whether companies announce further BTC purchases. What matters is whether the filings show that the acquisitions are permanent, taking into account financing costs, preferred dividends, note provisions, security interests, stock price declines, and listing compliance.

For stronger treasury companies, stable funding lines may preserve the hold-vs.-accumulate option. The same market can look different for weaker companies. Bitcoin may be the cleanest asset to sell, the easiest source of cash, or the clearest way to satisfy a modified loan agreement.

K Wave is currently an application level example of that second pass.

The company’s disclosures leave widespread government bond trading intact, but make it harder to ignore the downside mechanism. Bitcoin’s financial strategy is as durable as the balance sheet beneath it, and K Wave’s June 30 filing shows what happens when the balance sheet starts to point somewhere else.