Venice, the AI platform behind the VVV token, has raised $65 million in a Series A led by Dragonfly at a $1 billion equity valuation. This is the company’s first external capital raise. The company opted for shares rather than its own tokens, but the market is already buzzing with debate about what that choice means for VVV holders.

Series A investors received 8.98% equity, a VVV vesting grant of 1.5 million, and a guarantee to purchase an additional 5 million VVV over eight years. The package brings together Dragonfly, Coinbase Ventures, North Island Ventures, and other participants on both sides of Venice’s capital structure to hold shares and tokens in the same transaction.

Acquisition details of assets owned by the holder group Main restrictions Series A investor capital 8.98%, VVV granted 1.5 million, VVV 5 million guaranteed Legal ownership of Venice AI and token-linked upside Token exposure will be fixed over time and market Depends on the demand for VVV holders with public token staking access, exposure to DIEM mints, buy-and-burn mechanisms, and no direct legal ownership of Venice AI.VVV’s largest token position with over 30 million in the Venice Treasury. Alignment with public VVV holders Financial value depends on VVV market price Venice AI stockholders Stocks in the company Company upside, ownership, and contractual protections Not publicly liquid like VVVDIEM users Computing credits minted through VVV staking $1 of Venice computing access updated daily per DIEM Utility exposure, not ownership exposure

Venice’s own VVV page describes the token as the platform’s long-term deflationary capital asset. This creates a feedback loop where platform revenue buys and spends VVV, reducing supply and making the token scarce.

When you stake VVV, you will also be issued DIEM, which is a $1 worth of Venice computing access credits that are updated daily.

Eric Voorhees characterized the X round as “VVV and capital,” explaining that Venice financed growth with equity without touching VVV’s Treasury holdings.

He said Venice still holds more VVV than anywhere else, with over 30 million tokens out of a supply of over 80 million. Despite the token’s surge this year, neither Venice nor its team has sold VVV.

Venice plans to reduce its reliance on leased GPUs and build its own computing infrastructure, including its first data center. Voorhees said the resulting higher profit margins could make larger VVV burns possible. Increased profit margins fund more earning capacity, and more earning capacity funds larger burns.

The disconnect between stocks and tokens

Danclad Feist expressed skepticism, saying that while equity holders have legal protections, token holders are dependent on Venice continuing to buy back and burn their companies, so the split between tokens and shares in the deal is “terrible.”

This criticism centers on the fact that Venice itself sells VVV as a capital asset for its platform, creating a framework in which token holders expect something close to the company’s economics.

While both sides agree that Venice is a real business with real revenue and that revenue continues to grow, there are disagreements over which assets will earn it.

Equity holders own legal claims against Venice AI backed by contracts, while VVV holders own engineered economic claims built from staking, DIEM, and writing mechanisms that depend on Venice choosing to continue running.

Stockholders will have legal ownership of Venice AI and the governance rights specified in the transaction documents. VVV holders will receive staking access, DIEM mint passes, exposure to buy-and-burn mechanisms, and the ability to trade tokens on the open market.

Series A investors can now hold slices of both layers simultaneously through VVV grants and warrants.

The $1 billion stock valuation represents approximately 14.3 times Venice’s reported annual revenue. VVV trades at approximately $13.55, representing a market capitalization of approximately $637 million and a fully diluted value of approximately $1.54 billion, representing approximately 9.1x and 22.1x sales on these two metrics.

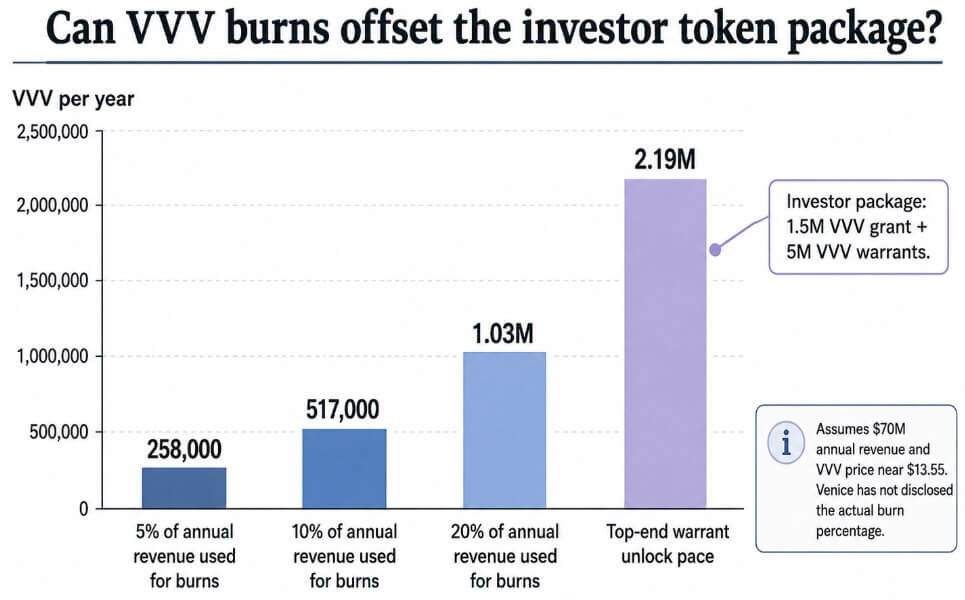

Whether Burn can offset the supply of new tokens will depend on the proportion of Burn that Venice keeps private. At 5% of annual income, Venice will retire approximately 258,000 VVV per year at current prices, rising to 517,000 and 1.03 million at 10% and 20%, respectively.

The investor package alone includes VVV 6.5 million in grants and warrants, which are phased in over a one-year lock and three-year vesting period.

Voorhees estimates that once fully exercised warrants begin to unlock, less than 6,000 VVV will be added to circulation per day, at a rate of approximately 2.19 million VVV per year at the highest value.

Goldman Sachs predicts AI capital spending to reach $765 billion in 2026 and $1.6 trillion by 2031, and computing builds of that scale tend to reward hardware owners rather than leasing companies.

Increasing GPU and data center capital is a standard move for companies at the Venice stage. Keeping VVV as the top public economy tier of equity rounds is still being discussed as part of cryptocurrencies.

how this will turn out

In the bullish case, Venice converts its equity raising into computing ownership quickly enough to expand its margins within the next 1-2 years.

As annual revenue continues to rise above the current $70 million run rate and the buy-and-burn volume increases accordingly, VVV’s token-linked dilution from Series A grants and warrants will ultimately be less than the amount the burn will retire.

Venice maintains its position as the largest VVV holder and the token begins trading like a credible claim to the platform’s growth.

In a bearish case, Venice’s stock value will exceed VVV. As the company continues to expand, its computing investments pay off, with much of the upside flowing to stockholders through valuation multiples that no token can match.

Compared to VVV’s fully diluted value of $1.54 billion, Burns remains modest and the Series A ensures on-time unlocking. The market has begun to price VVV as a staking and DIEM access asset, but this is a narrower role than fully asserting Venice’s corporate value.

Scenarios What Happens Who Gains the Most Value What It Means for VVV Bull Case: Tokens Gain Flywheel Equity Funds Calculate Ownership, Margins Improve, Returns Increase, Massive Burns Reduce VVV Supply Faster than Token Link Dilution Amplifies. Both VVV holders and stockholders benefit. VVV trades like a reliable income-linked asset. Base case: Two tiers coexist Venice grows, but VVV is still primarily staking, DIEM, and burn exposed assets rather than direct representation of companies. Splitting equity and token holders VVV works, but it is discounted compared to equity due to weaker rights. Bearish case: Venice becomes more valuable as a company as its stock exceeds its token value, but Burn remains modest compared to FDV and investors are guaranteed unlocking over time. Shareholder VVV will be repriced as an access asset rather than a full claim. Growth of Venice. Black Swan: Future strategies, regulations, or funding choices that weaken the role of the token reduce the importance of VVV to the platform. Shareholder VVV loses the “capital asset” narrative and trades primarily in utilities.

Venice has already done the hard part of what cryptocurrencies say they want to do: build a real product, generate real revenue, issue public tokens, and then raise external capital for the first time.

For every dollar added to Venice’s revenue, it becomes more urgent to know whether that dollar is reflected in VVV’s price, Venice AI’s stock value, or unevenly distributed between the two.