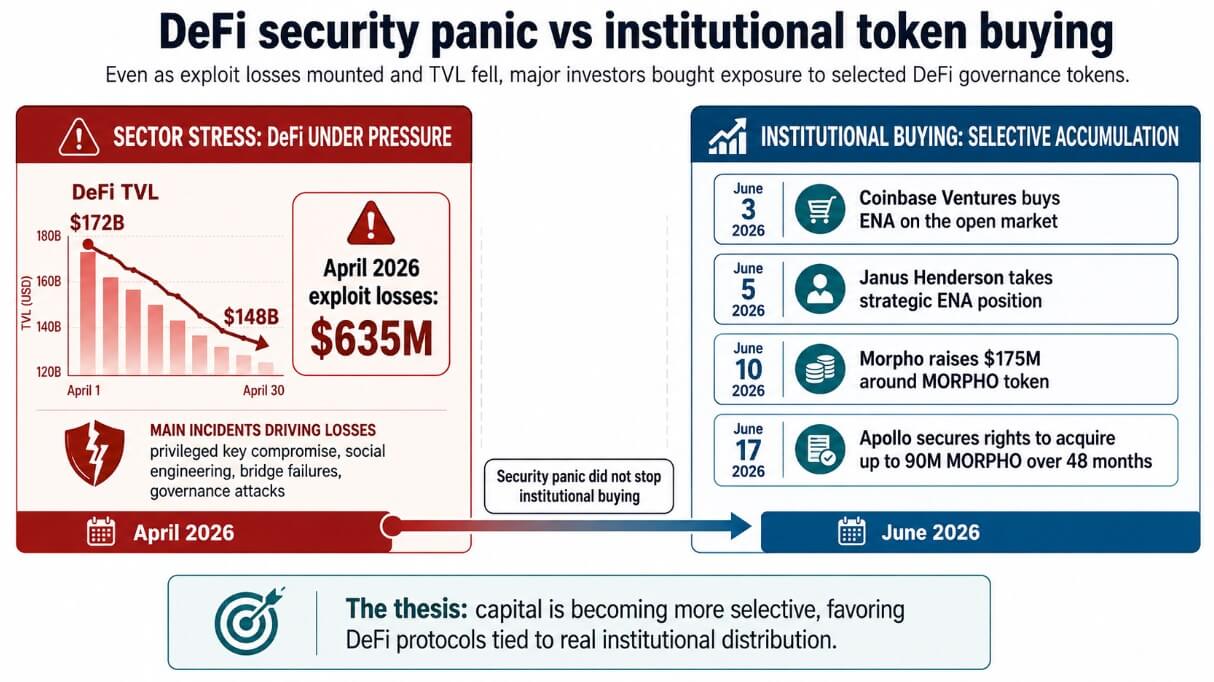

DeFi’s total value locked (TVL) fell from $172 billion to $148 billion as the sector recorded $635 million in exploit losses in April alone. Coinbase Ventures purchased Ethena’s ENA tokens on the open market, Janus Henderson acquired a unique strategic ENA position, and Morpho closed a $175 million round structured entirely around MORPHO tokens.

Apollo has separately secured the right to acquire up to 90 million MORPHO tokens over a 48-month period.

The bet these investors are making is that governance tokens attached to DeFi protocols that are actually distributed to institutions will be revalued as financial infrastructure, and that security panic will accelerate that outcome by removing weaker protocols from execution.

Bets on infrastructure

Morpho reports more than $11 billion in deposits and its institutional users include Bitwise, Galaxy, Anchorage Digital, Coinbase, Kraken, and Binance.

Apollo’s token acquisition agreement was limited to 90 million MORPHO over a 48-month period, with transfer and trading restrictions structured through open market purchases, OTC transactions, or other contractual arrangements.

Fortune reported that the $175 million raise could bring the protocol’s value up to $2 billion. This number is completely derived from the market value of the token.

ENA sits at the governance layer of the synthetic dollar protocol routed through Coinbase’s over 100 million users, with Coinbase already acting as Ethena’s primary custodian, wallet provider, and perpetual exchange.

Meanwhile, Janus Henderson combines ENA’s position with plans to use USDe for Treasury cash management and explore tokenized CLO collateral through its own and Centrifuge’s infrastructure.

With the 10-year US Treasury yield around 4.55% and the Fed’s target range of 3.50% to 3.75%, which most economists expect to remain until the end of 2026, there is an economic relevance for stablecoin yields, tokenized US Treasuries, and on-chain credit markets that makes these positions understandable for traditional asset managers.

USDe has a market cap of about $4.5 billion and is up 13% in 30 days, while ENA itself has a market cap of about $750 million and trades close to $0.08.

Protocol/Token Infrastructure Exposure Institutional Links Key Adoption Indicators Token Notes Ethena/ENA Synthetic Dollar, Stablecoin Yield, Collateral, Treasury Cash Management Coinbase, Janus Henderson, Anchorage USD Market Cap Approximately $4.5 Billion, Up 13% in 30 Days ENA Price Near $0.08. Adoption is not clearly reflected in token valuation Morpho / Morpho On-chain lending, credit markets, vault infrastructure Apollo, Paradigm, A16Z, Circle Ventures, Van Eck, Coinbase, Kraken, Binance More than $11 billion in deposits. TVL $6.43 billion. $3.43 billion active loan governance rights not equivalent to equity, cash flow receivables, or legal ownership

Why security panics make theories clearer

The wave of incidents in April spanned privileged key compromise, social engineering, bridge failures, governance surface attacks, and external dependencies.

Protocols with institutional distribution, professional custody integration, transparent collateral structures, and real demand from exchanges and asset managers come with different risk profiles.

If capital continues to drive down prices on DeFi’s weakest tiers, protocols already embedded in organizations’ workflows will absorb flows and outflows from weaker venues.

Janus Henderson, Apollo, Circle Ventures, and VanEck each took positions in DeFi infrastructure tokens as security concerns accelerated decoupling between protocols tied to real institutional demand, but these DeFi TVL numbers have historically tracked as capital has become more selective about which rails it trusts.

ENA and MORPHO give holders governance rights over the protocol outside of what either token conveys, such as ownership of Ethena Labs or Morpho Association, legal claim to cash flows, and control of assets.

Betting on these tokens will only work if adoption leads to token demand, governance relevance, or reliable value capture.

According to DefiLlama, MorphoBlue generated approximately $39 million in total protocol revenue in the second quarter, with $3.43 billion in active loans flowing to liquidity providers and vault managers against a TVL of $6.43 billion.

Coinbase and Janus Henderson offer Ethena a distribution that most DeFi protocols do not have access to, and USDe’s market cap has increased by about 13% in 30 days to about $4.49 billion.

However, ENA fell about 10% on the day of Janus’ announcement, leaving the token at nearly $0.08 and a market cap of about $750 million.

ENA buyers are positioning on the convergence between institutional adoption and token value that the market has not yet priced in.

Shape of next cycle

If Coinbase, Janus Henderson, Apollo, Circle, and VanEck normalize DeFi-backed cash and credit products through existing channels, and security panic continues to funnel capital to top-tier protocols, ENA and MORPHO will be valued more as governance assets than infrastructure to handle actual institutional volumes.

USDe will then retest a significantly larger supply base, with Morpho deposits moving towards $18 billion and $25 billion, with both tokens trading as strategic assets with claims on the rails below.

If another significant exploit, depegging event, or regulatory restriction suspends the institution’s distribution, governance token ownership will prove to have always been decoupled from the protocol’s economics.

In this scenario, USDe supply would decline by 30% to 50%, MORPHO would be sold despite continued use of the protocol, and the disconnect between retaining governance rights and capturing value from the protocol would remain large.

Scenario What Happens Impact of USDe/ENA Impact of Morpho/MORPHO Greater Harvest Bull Case Institutional distributions expand, security panic concentrates capital in top protocols USDe retests larger supply base. ENA assesses governance of synthetic dollar infrastructure Deposits heading for $18-25 billion. MORPHO Trades as Strategic Governance Exposure Bearish Case for Governance Tokens to Be an Infrastructure Asset Large-scale exploit, depeg, or regulation suspends adoption USDe supply declines by 30%-50%. ENA remains decoupled from adoption MORPHO is sold despite continued use of the protocol Base case Adoption grows, but token value capture remains uncertain USDe grows, but ENA repricing is uneven Morpho usage increases, but value generation remains uncertain Infrastructure wins and token holders may not be a black swan Core protocol, custody, collateral, or governance failure ENA loses infrastructure premium Failure of the “trusted rail” theory where Morpho’s governance becomes a liability

Apollo, Paradigm, a16z, Janus Henderson, and Coinbase Ventures each made separate bets on whether their chosen rail would provide enough institutional size to govern the rails worth owning.

Whether ownership of a token brings us closer to the economic value flowing through the underlying protocol is the real open question of this cycle.